How to double your money in the UK

Verdict

For higher-rate taxpayers, pension contributions typically produce larger net retirement value than an equivalent ISA — driven by 40% relief on entry vs 20% tax on drawdown.

Confidence: High

Break point: This verdict changes if your expected drawdown tax rate exceeds your contribution relief rate, or if you need access to savings before age 57.

The tax decision

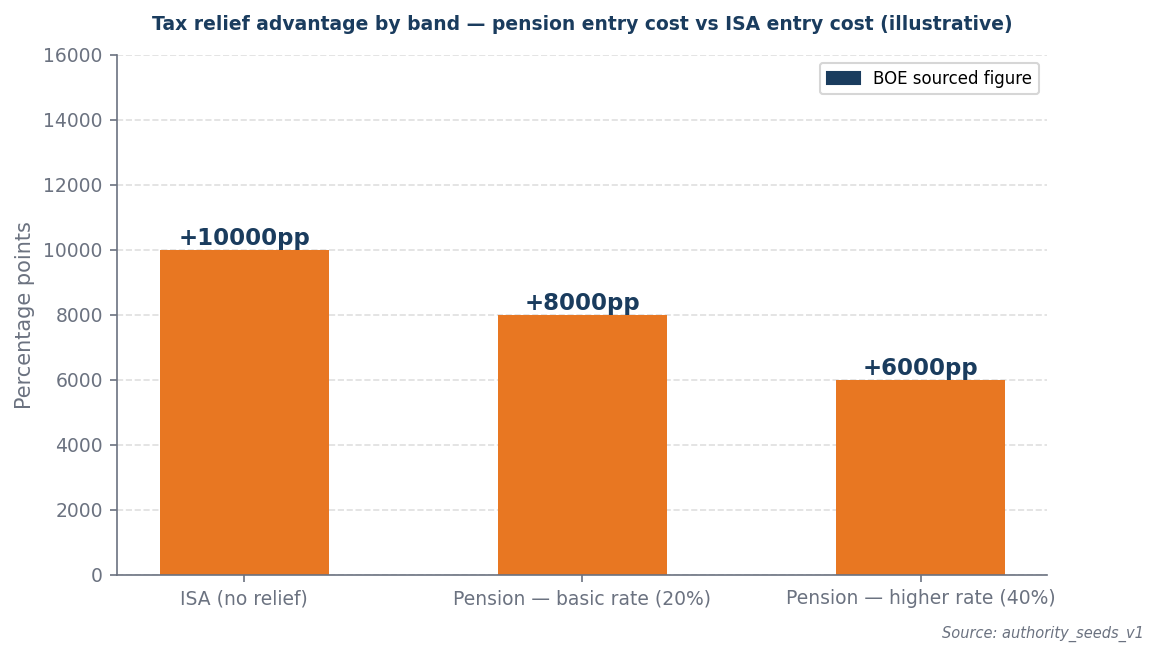

Higher-rate taxpayers get 40p of relief for every £1 contributed — the ISA cannot match that on entry cost alone.

Higher-rate taxpayers should prioritize pension contributions over ISAs due to the significant tax relief received at the point of entry, where a 40% relief on contributions effectively boosts the initial investment, compared to the 20% tax applied during ISA withdrawals. For individuals in the higher tax band, this means that every £100 contributed to a pension only costs them £60 after tax relief, maximizing their investment potential. Conversely, when drawing down from an ISA, the full amount is subject to taxation, diminishing the net retirement value. Therefore, for those expecting to withdraw in a lower tax band, the pension's upfront tax advantage outweighs the ISA's tax-free withdrawals, making pensions the superior choice for maximizing retirement savings.

The tax backdrop

The pension wins on entry cost; the ISA wins on flexibility. Which matters more depends entirely on your horizon and tax band.

The UK tax environment, characterized by a frozen personal allowance of £12,570 and an unchanged higher rate threshold until 2028, intensifies the pension versus ISA decision for higher-rate taxpayers, as the lack of adjustments means more income will be taxed at higher rates without the benefit of increased allowances. In this context, pension contributions become particularly advantageous, as they provide a 40% tax relief at the point of contribution, significantly enhancing the initial investment compared to an ISA, which is subject to 20% tax upon withdrawal. Consequently, the effective net retirement value of pension contributions is likely to exceed that of an equivalent ISA investment, making the choice of pension over ISA more consequential for those in higher tax brackets. This backdrop underscores the importance of strategic tax planning in maximizing retirement savings.

Worked example

Assumptions (illustrative): £10,000/yr contribution · 7.0% assumed return · Basic rate taxpayer (20% relief) · 25% tax-free lump sum on drawdown

| Year | Pension fund | ISA fund | Who is ahead |

|---|---|---|---|

| Year 1 | £10,700 | £8,560 | Pension ahead by £2,140 |

| Year 2 | £22,149 | £17,719 | Pension ahead by £4,430 |

| Year 3 | £34,399 | £27,520 | Pension ahead by £6,879 |

| Year 4 | £47,507 | £38,006 | Pension ahead by £9,501 |

| Year 5 | £61,533 | £49,226 | Pension ahead by £12,307 |

| Year 6 | £76,540 | £61,232 | Pension ahead by £15,308 |

| Year 7 | £92,598 | £74,078 | Pension ahead by £18,520 |

| Year 8 | £109,780 | £87,824 | Pension ahead by £21,956 |

| Year 9 | £128,164 | £102,532 | Pension ahead by £25,632 |

| Year 10 | £147,836 | £118,269 | Pension ahead by £29,567 |

| Year 11 | £168,885 | £135,108 | Pension ahead by £33,777 |

| Year 12 | £191,406 | £153,125 | Pension ahead by £38,281 |

| Year 13 | £215,505 | £172,404 | Pension ahead by £43,101 |

| Year 14 | £241,290 | £193,032 | Pension ahead by £48,258 |

| Year 15 | £268,881 | £215,104 | Pension ahead by £53,777 |

| Year 16 | £298,402 | £238,722 | Pension ahead by £59,680 |

| Year 17 | £329,990 | £263,992 | Pension ahead by £65,998 |

| Year 18 | £363,790 | £291,032 | Pension ahead by £72,758 |

| Year 19 | £399,955 | £319,964 | Pension ahead by £79,991 |

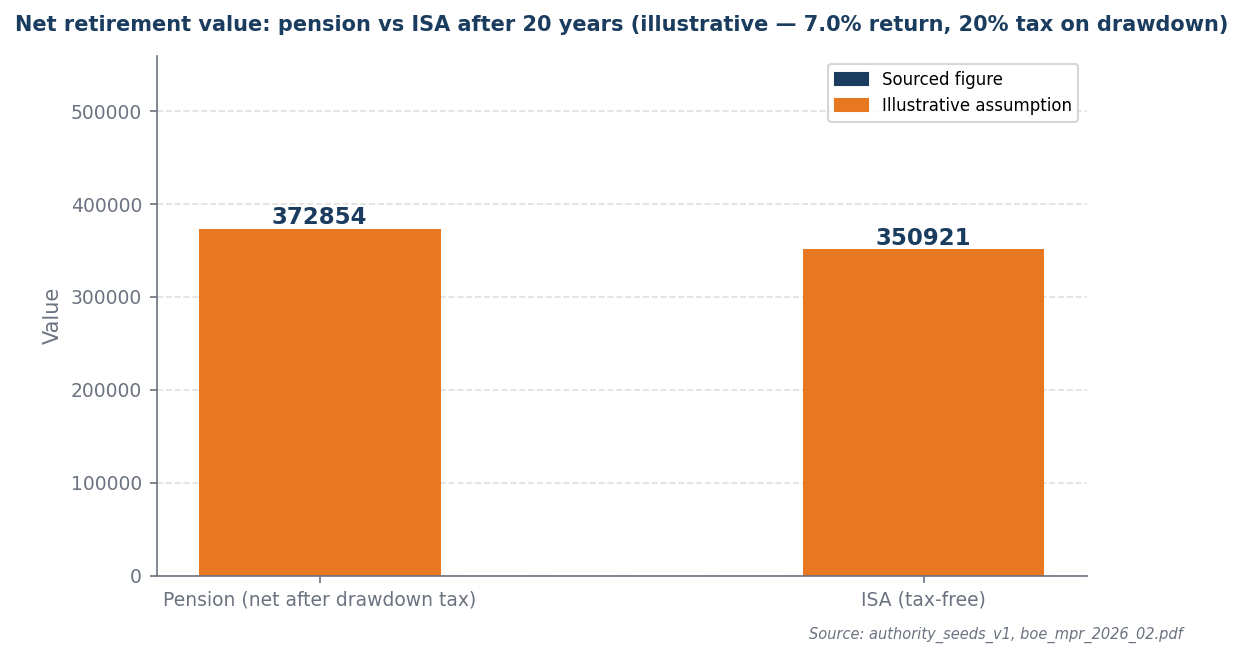

| Year 20 | £438,652 | £350,921 | Pension ahead by £87,731 |

By year 20, the pension fund (£438,652) exceeds the ISA (£350,921) by £87,731 — driven by tax relief on entry. This assumes drawdown tax at 20% and 25% tax-free lump sum.

This comparison flips if the drawdown tax rate exceeds the contribution relief rate, or if the investment horizon is shorter than 20 years.

When this flips

This flips only when the expected drawdown tax rate exceeds the contribution relief rate, removing the pension tax advantage. A minimum investment horizon of 20 years is required to effectively assess the long-term benefits.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Basic rate taxpayer | ISA or pension roughly equal | 20% relief in, 20% tax out — net effect is neutral on tax |

| Higher rate taxpayer | Pension wins clearly | 40% relief on entry vs 20% tax on drawdown = large net gain |

| Need flexibility before retirement | ISA preferred | Pension locks money until 57 — ISA is fully accessible |

| Both available | Max pension to higher rate band, ISA for rest | Capture full relief then preserve flexibility |

Sources and provenance

- authority_seeds_v1

- boe_mpr_2026_02.pdf

Data as of: 2026-04-28

Capital at risk. The value of investments can fall as well as rise. This article contains affiliate links. We may earn a commission if you click through and open an account. .