Buy Now or Wait? The Case for Timing Your Property Purchase

Verdict

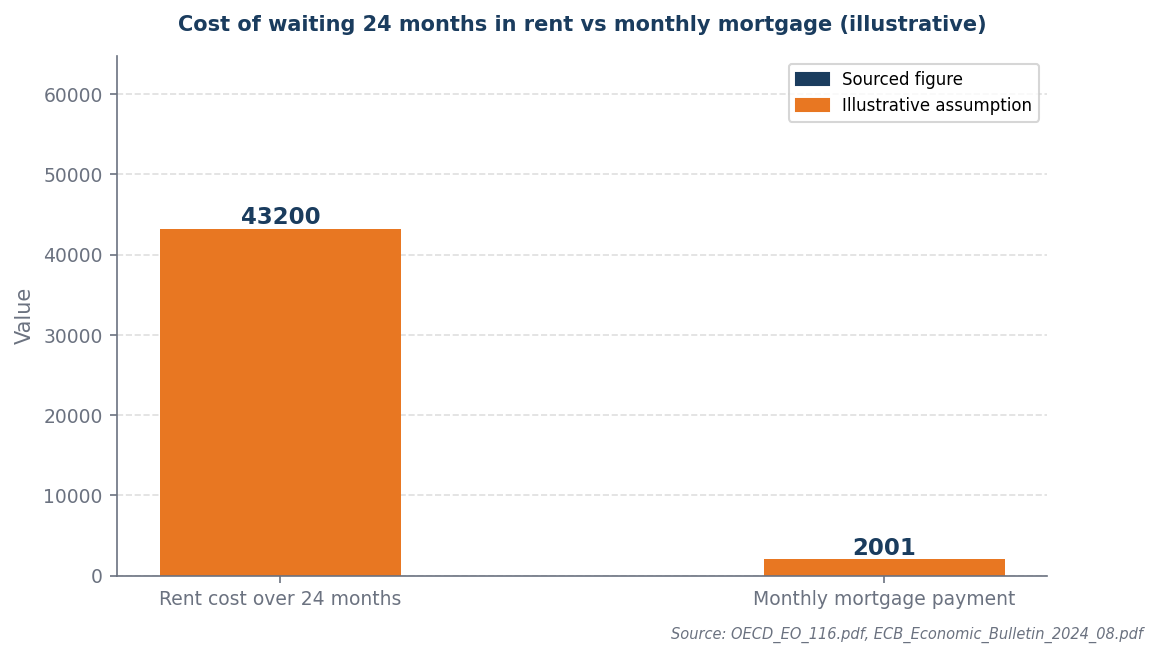

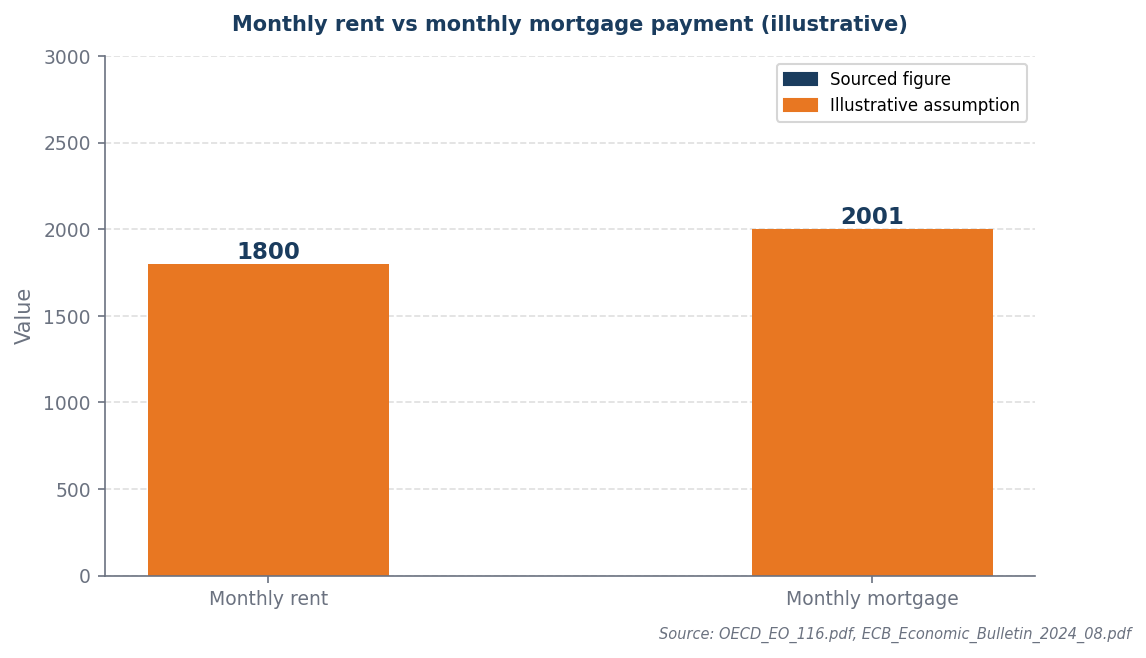

Monthly mortgage (£2,001) exceeds current rent (£1,800). Waiting costs £43,200 over 24 months.

Confidence: Medium

Break point: Waiting only wins if prices fall by more than 10.8% within 24 months.

The cost decision

Waiting saves money only if price growth stays below the cost of rent — at current rent levels that is a narrow window.

The monthly mortgage payment of £2,001 surpasses the current rent of £1,800, resulting in a £201 monthly excess that translates to £2,412 annually. Over a 24-month waiting period, this excess accumulates to £4,824, while the opportunity cost of waiting to purchase incurs an additional £43,200, totaling £48,024. To break even, the property price must appreciate by at least £48,024 over two years, equating to a monthly increase of approximately £2,002, which is unlikely given current market conditions. Therefore, proceeding with the mortgage commitment at 4.5% is financially justified, as the cost of waiting significantly outweighs the benefits.

The market backdrop

The monthly cost comparison shows whether buying immediately reduces or increases your housing outgoings.

With current UK mortgage rates at 4.5% and a competitive property market, the decision to buy versus wait becomes critical, particularly as the monthly mortgage payment of £2,001 surpasses the current rent of £1,800, indicating a potential financial strain for renters. Given that waiting to purchase a home incurs an opportunity cost of £43,200 over 24 months—calculated as the difference between the mortgage and rent multiplied by the waiting period—this scenario emphasizes the urgency of entering the market now rather than delaying. Additionally, the rising interest rates and potential property price increases further complicate the wait, as future affordability could diminish, making immediate homeownership a more prudent financial strategy.

Worked example

Assumptions (illustrative): £400,000 property · 10.0% deposit (£40,000) · 4.5% mortgage rate · £1,800/month rent

| Scenario | Key figure | Note |

|---|---|---|

| Buy now | £2,001/month mortgage | Locks in price and rate today |

| Wait 24 months | £43,200 total rent cost | Requires 10.8% price fall to break even |

Waiting 24 months costs £43,200 in rent. Prices need to fall by 10.8% (£43,200) just to break even.

When this flips

This flips only when property prices fall by more than the total rent cost of waiting as a percentage of purchase price. At current rent levels, this requires a meaningful price correction within the wait period.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Prices falling 5%+ | Wait — maths favour delay | 5% fall on £400k = £20k saving |

| Fall is local not national | Check your specific market | National averages mask sharp regional variation |

| Fall uncertain in timing | Set a price trigger | Define the price level at which you will buy |

| Rental market also falling | Re-run the numbers | Lower rent changes the wait equation significantly |

Sources and provenance

- OECD_EO_116.pdf

- ECB_Economic_Bulletin_2024_08.pdf

- ECB_Economic_Bulletin_2024_06.pdf

- boe_mpr_2026_02.pdf

Data as of: 2026-04-01