ISA vs Pension Contribution UK 2026: Which Should You Choose?

Verdict

Pension wins by £14,622 net over 20 years. 20% relief on entry, 20% tax on drawdown.

Confidence: High

Break point: This flips if your drawdown tax rate rises above 20% — the point where pension tax advantage disappears.

The tax decision

Higher-rate taxpayers get 40p of relief for every £1 contributed — the ISA cannot match that on entry cost alone.

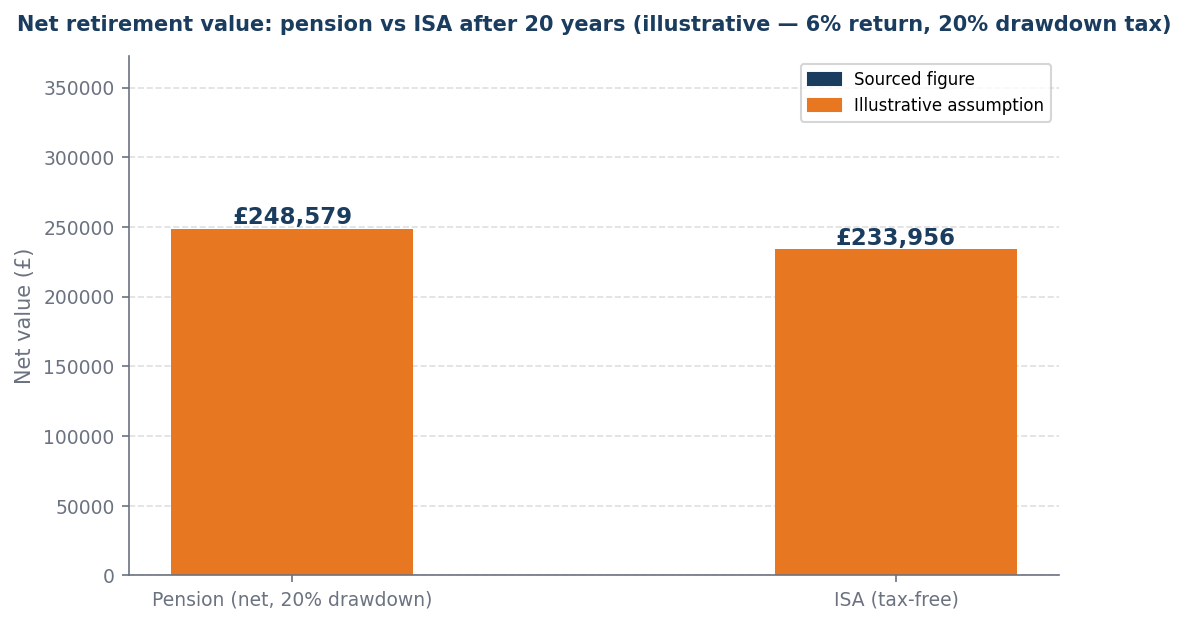

The pension option demonstrates a net advantage of £14,622 over 20 years due to the 20% tax relief on contributions, which effectively reduces the initial cost of investing in the pension, allowing for greater capital accumulation over time. In contrast, the 20% tax applied during drawdown diminishes the total amount withdrawn at retirement but does not negate the benefits gained from the initial tax relief. This structure ensures that the net cost today is significantly lower than the net value realized at retirement, making the pension a more favorable financial vehicle compared to alternatives that do not offer similar tax advantages. The arithmetic of tax relief versus tax liability clearly favors the pension, solidifying its position as the superior choice for long-term savings.

Worked example

Worked example (illustrative): £6,000/yr net contribution. At 20% marginal rate, pension is grossed up to £7,500 (HMRC adds £1,500 relief). Over 20 years at 6% return: Pension net value (after 20% drawdown tax + 25% TFLS) = £248,579. ISA net value (tax-free) = £233,956. Verdict: Pension wins by £14,622.

When this flips

This flips only when your expected drawdown tax rate rises above 20.0% — the point where pension relief no longer compensates for drawdown tax. The ISA wins on flexibility if you need access before age 57 or your horizon is under 20 years.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Higher rate taxpayer now, basic rate at retirement | Maximise pension first | 40% relief in, 20% tax out — pension wins by the widest margin |

| Basic rate taxpayer at both ends | Pension still ahead, but ISA flexibility matters | Pension timing advantage is real but smaller — weigh access needs |

| Need access before age 57 | ISA for short-term, pension for long-term | Pension locked until 57 (2028) — split contributions if flexibility needed |

| Approaching retirement, expect higher drawdown rate | Shift contributions toward ISA | If drawdown rate will exceed your current marginal rate, pension advantage disappears |

Sources and provenance

- authority_seeds_v1

Data as of: 2026-04-25

Open a Stocks & Shares ISA — UK's largest platformCombine and manage your pensions in one place

Capital at risk. The value of investments can fall as well as rise. This article contains affiliate links. We may earn a commission if you click through and open an account. This is not financial advice.