Lump Sum: Invest or Pay Down Your Mortgage?

Verdict

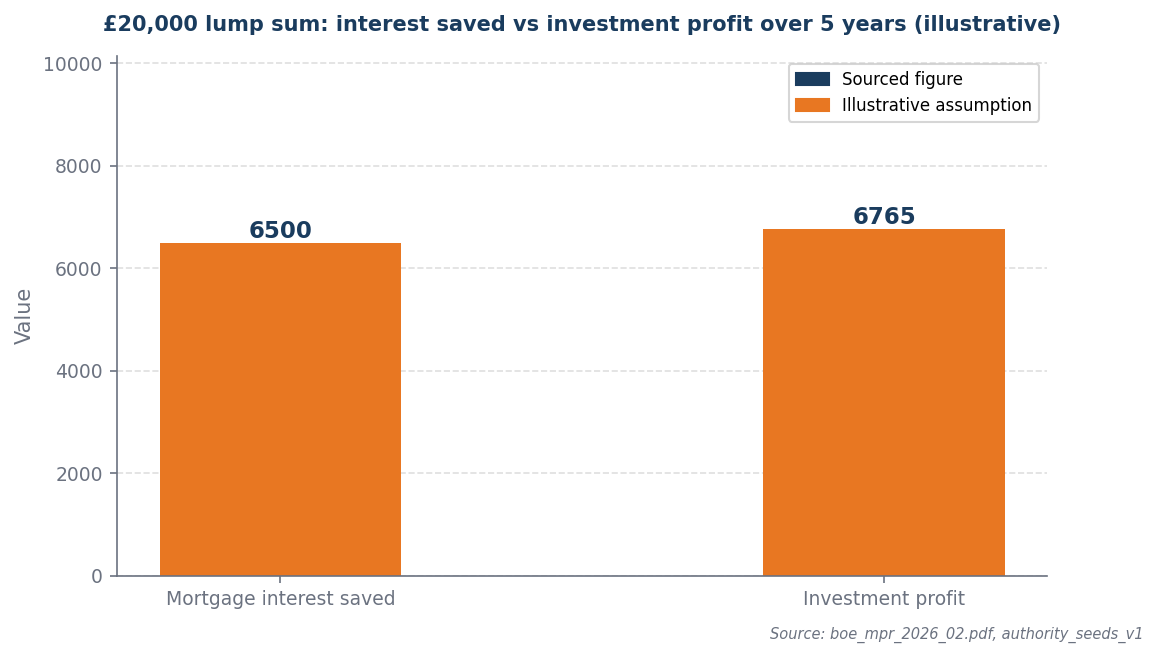

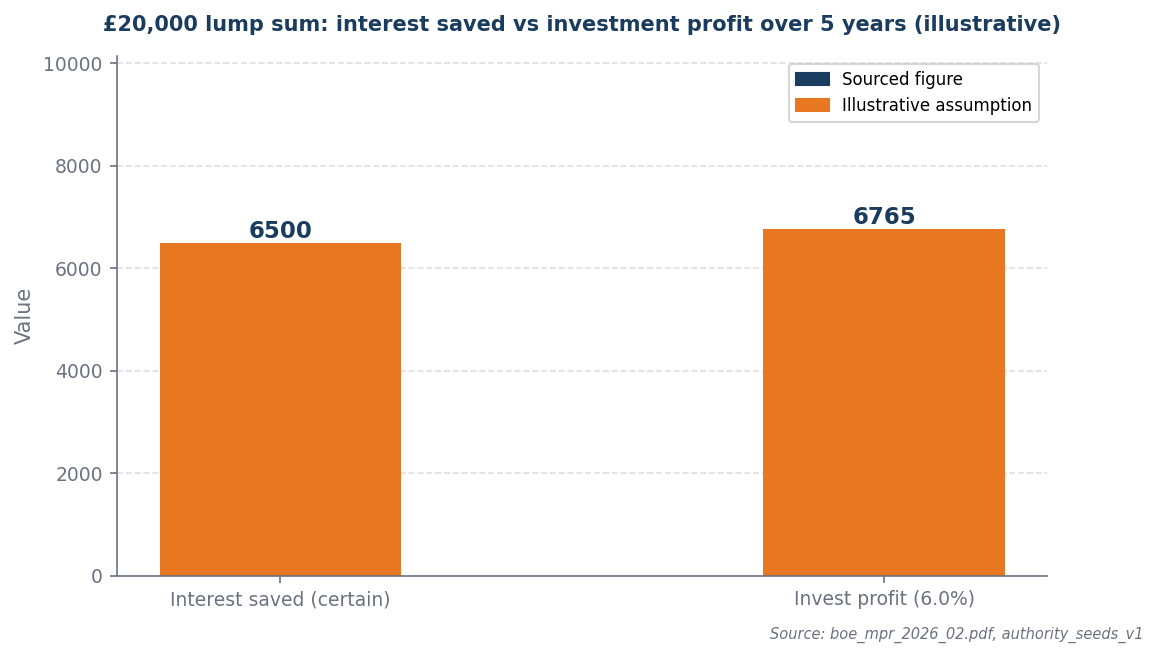

Paying down the mortgage saves £6,500 — more certain than the £6,765 investment profit at 6.0%.

Confidence: High

Break point: Investing only wins if returns consistently exceed 8.5%.

The rate decision

A lump sum on the mortgage gives a guaranteed return equal to your rate — investing only wins if returns consistently clear that hurdle.

Paying down the mortgage is the superior financial decision, yielding a guaranteed savings of £6,500, compared to the uncertain £6,765 profit from investing at a 6.0% return. The 6.5% mortgage rate serves as a hurdle rate, meaning that any investment must exceed this rate to be worthwhile; since the expected return is only 6.0%, it falls short by 0.5 percentage points. This gap underscores the risk of investing over the assured benefit of reducing debt, making the mortgage payoff the more prudent choice for a lump sum allocation. Prioritizing debt reduction eliminates the risk associated with market fluctuations, ensuring a more favorable financial outcome.

The return backdrop

Over a short horizon the certain interest saving wins; over a long horizon compounding can overcome the mortgage rate.

With UK mortgage rates at 6.5%, the decision to pay down a mortgage becomes particularly consequential as the guaranteed savings from reducing debt are more attractive than potential investment returns, which are inherently uncertain. In this context, paying down the mortgage yields a certain saving of £6,500, which is more reliable than the projected £6,765 profit from investing at a lower rate of 6.0%, where actual returns can fluctuate. This stark comparison underscores the financial prudence of prioritizing debt reduction in a high-rate environment, where the risk-adjusted returns on investments may not justify the opportunity cost of maintaining higher mortgage debt. Thus, the certainty of saving on interest payments outweighs the potential, yet uncertain, gains from alternative investments.

Worked example

Assumptions (illustrative): £20,000 lump sum · 6.5% mortgage rate · 6.0% assumed return · 5-year horizon

| Option | Value after 5 years | Gain above lump sum |

|---|---|---|

| Pay down mortgage | £6,500 saved | £6,500 (certain) |

| Invest lump sum | £26,765 | £6,765 (at 6.0%) |

Over 5 years, investing produces £265 more. The investment figure assumes 6.0% p.a. — not guaranteed.

When this flips

This flips only when investment returns consistently exceed 8.5% over at least 5 years. Below this threshold, the certain interest saving wins.

What to do next

| Your situation | Action | Why |

|---|---|---|

| High rate environment | Pay down mortgage first | 6.5% guaranteed saving is hard to beat |

| Investment return below rate | Pay down mortgage | No risk-free return exceeds this rate |

| Partial investment case | Pay down then invest | Clear the expensive debt first |

| Rate expected to fall | Revisit in 12 months | Future rate path changes the calculus |

Sources and provenance

- boe_mpr_2026_02.pdf

- authority_seeds_v1

Data as of: 2026-04-01