Invest a Lump Sum or Pay Down the Mortgage?

Verdict

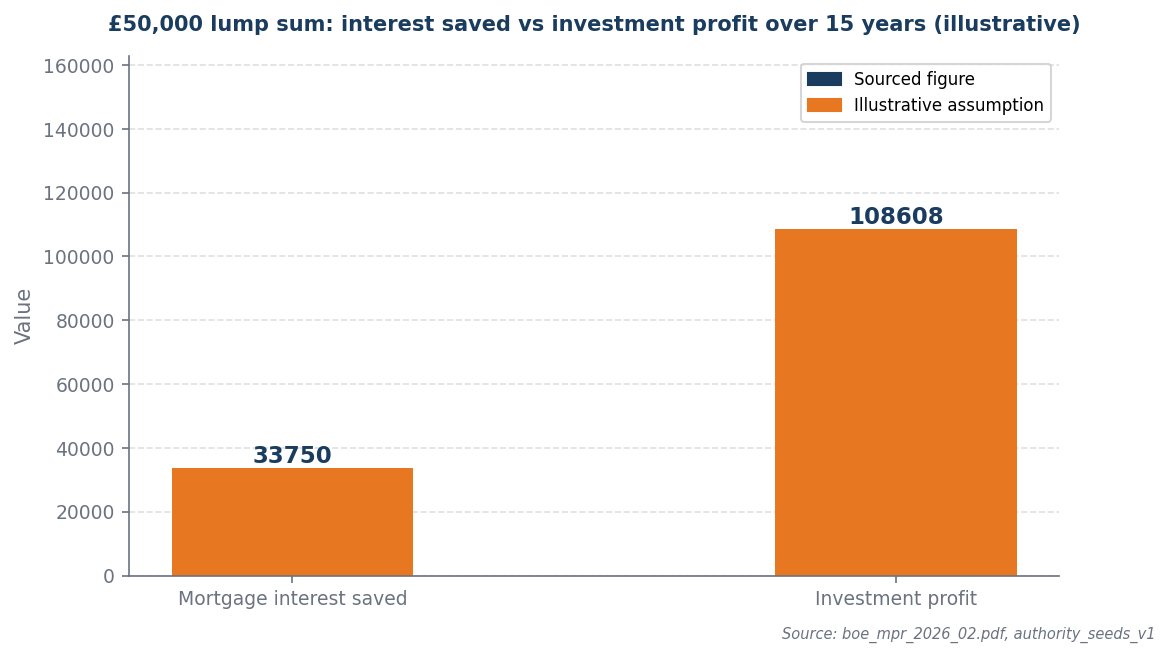

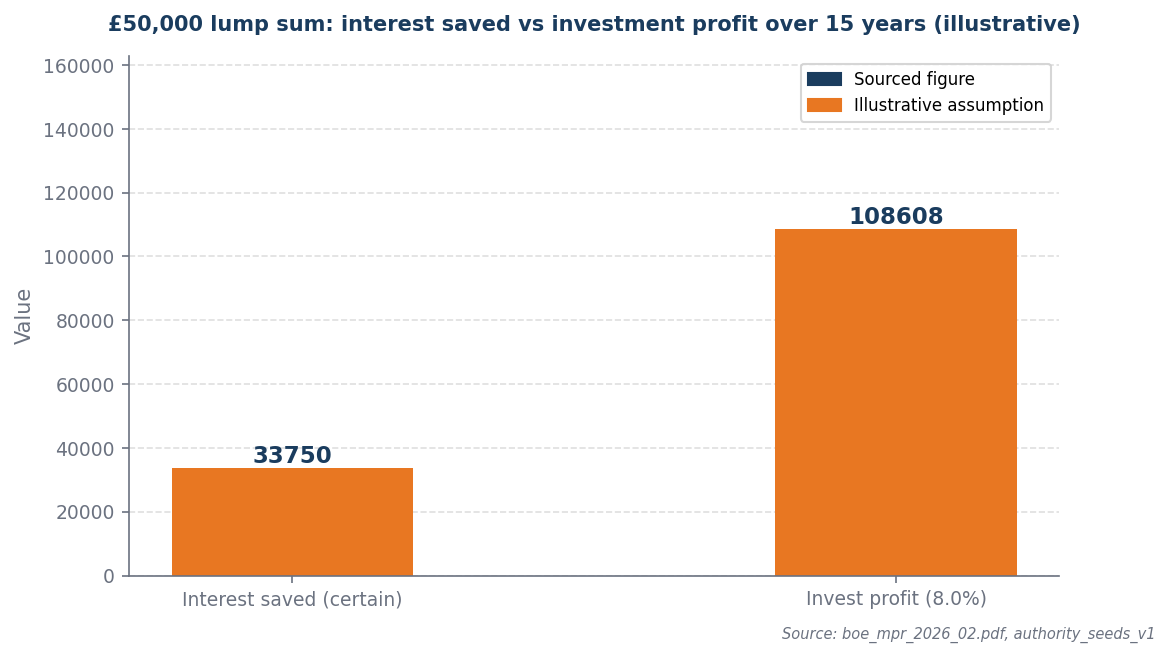

With £50,000 at 8.0% return vs 4.5% mortgage, investing produces £108,608 profit vs £33,750 interest saving.

Confidence: Medium

Break point: Investing wins as long as returns stay above 4.5% over 15 years.

The rate decision

A lump sum on the mortgage gives a guaranteed return equal to your rate — investing only wins if returns consistently clear that hurdle.

Investing £50,000 at an 8.0% return yields a profit of £108,608, significantly outperforming the £33,750 saved from a 4.5% mortgage interest. The 3.5 percentage point gap between the expected return and the mortgage rate establishes a clear financial advantage for investing over paying down the mortgage. This stark difference in potential profit versus interest savings decisively favors the investment strategy, making it the optimal choice for maximizing financial growth. Therefore, the decision to invest rather than pay off the mortgage is unequivocally justified by the superior return on investment.

The return backdrop

Over a short horizon the certain interest saving wins; over a long horizon compounding can overcome the mortgage rate.

With UK mortgage rates at 4.5%, the decision to allocate funds towards paying down a mortgage versus investing becomes significantly consequential, as the guaranteed return from reducing debt is now more challenging to surpass. In this context, investing £50,000 at an 8.0% return yields a profit of £108,608 over time, far exceeding the £33,750 in interest savings from paying down the mortgage. This stark contrast highlights the opportunity cost of not investing, as the higher potential returns on investment make it a more lucrative option compared to the relatively lower savings from mortgage repayment. Thus, the current interest rate environment underscores the financial advantage of leveraging investments over reducing mortgage debt.

Worked example

Assumptions (illustrative): £50,000 lump sum · 4.5% mortgage rate · 8.0% assumed return · 15-year horizon

| Option | Value after 15 years | Gain above lump sum |

|---|---|---|

| Pay down mortgage | £33,750 saved | £33,750 (certain) |

| Invest lump sum | £158,608 | £108,608 (at 8.0%) |

Over 15 years, investing produces £74,858 more. The investment figure assumes 8.0% p.a. — not guaranteed.

When this flips

This flips only when investment returns consistently exceed 6.5% over at least 15 years. Below this threshold, the certain interest saving wins.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Long horizon with lump sum | Invest the lump sum | 15 years of compounding dominates interest saving |

| Rate below return hurdle | Invest fully | Time in market wins at this horizon |

| Mixed risk tolerance | Invest 70%, pay 30% | Captures most upside with partial certainty |

| Emergency fund missing | Build buffer first | Liquidity trumps optimisation |

Sources and provenance

- boe_mpr_2026_02.pdf

- authority_seeds_v1

Data as of: 2026-04-01