Cash ISA vs Stocks ISA: Which is Better Now?

Verdict

Stocks ISA wins

Confidence: High

Break point: Equity return must stay above 5.2% every year over 10 years.

The rate that changes everything

The gap between stocks ISA and cash ISA terminal value widens significantly over longer horizons — compounding is the deciding factor.

The break-even equity return of 5.2% is the critical threshold that determines the superiority of the Stocks ISA over the Cash ISA; returns below this rate favor the Cash ISA, while returns above it decisively benefit the Stocks ISA. Given the current Cash ISA rate of 5.2%, any equity return that exceeds this figure will yield higher overall returns, making the Stocks ISA the clear winner for investors seeking growth. Therefore, if you anticipate a return above 5.2%, allocate your funds to the Stocks ISA; otherwise, the Cash ISA remains the safer choice. Focus solely on this break-even point to guide your investment strategy.

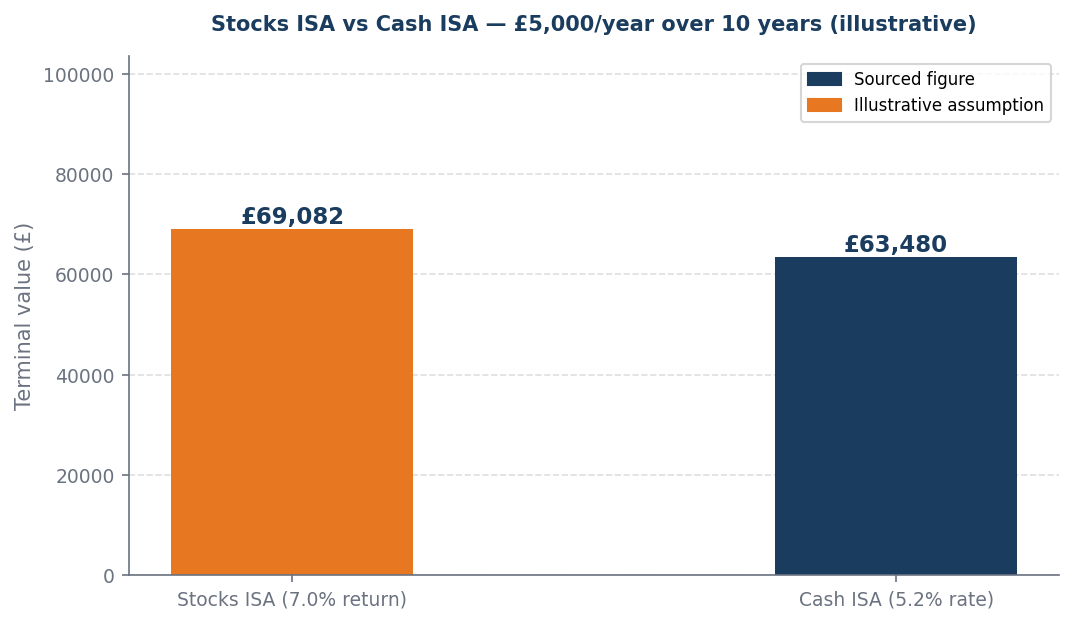

Worked example

Worked example (illustrative): £5,000/year invested over 10 years. At 7.0% equity return: Stocks ISA = £69,082. At 5.2% cash ISA rate: Cash ISA = £63,480. Stocks ISA produces £5,603 more. Verdict: Stocks ISA wins. Break-even equity return: 5.2%.

When this flips

This flips only when equity returns must stay above 5.2% every year over the full 10-year horizon. If the horizon shortens or the cash ISA rate rises, the attractiveness of equities diminishes relative to safer investments.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Equity return above break-even | Stocks ISA | Expected return clears the hurdle — compounding wins over the horizon |

| Equity return below break-even | Cash ISA | The certain cash rate beats the uncertain equity return at this level |

| Short horizon under 5 years | Lean cash ISA | Insufficient time to smooth equity volatility — certainty has higher value |

| Long horizon over 15 years | Lean stocks ISA | Compounding over a long runway makes the break-even much easier to clear |

Sources and provenance

- OECD_EO_116.pdf

- boe_mpr_2026_02.pdf

Data as of: 2026-04-06