Should You Buy a House Now or Wait in 2026?

Verdict

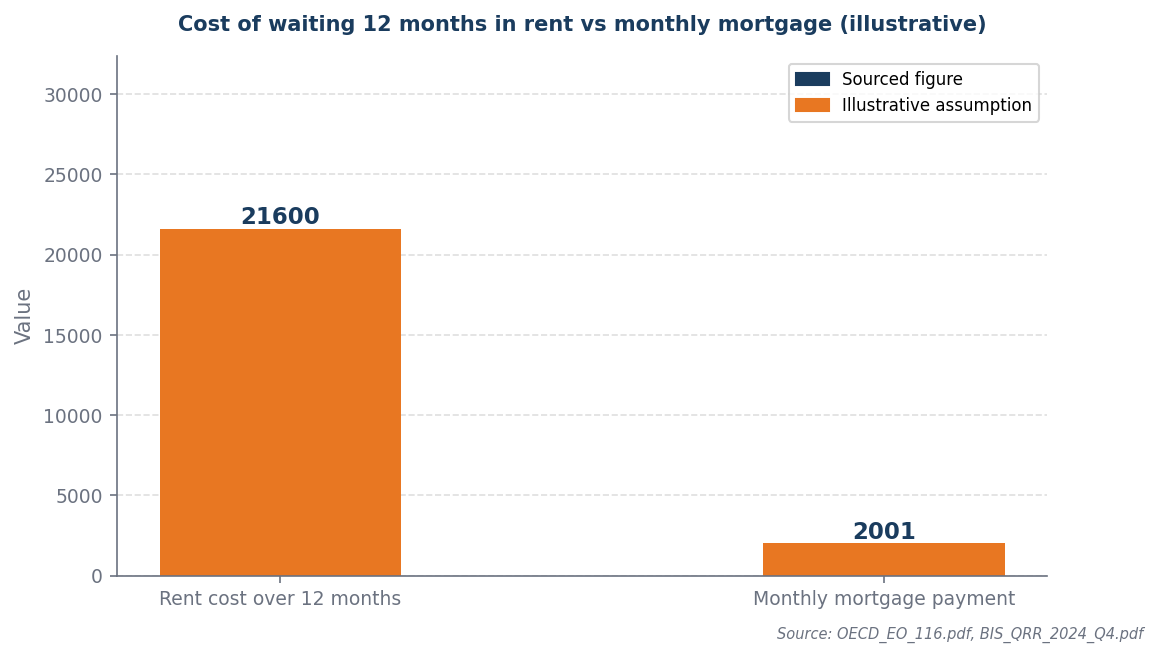

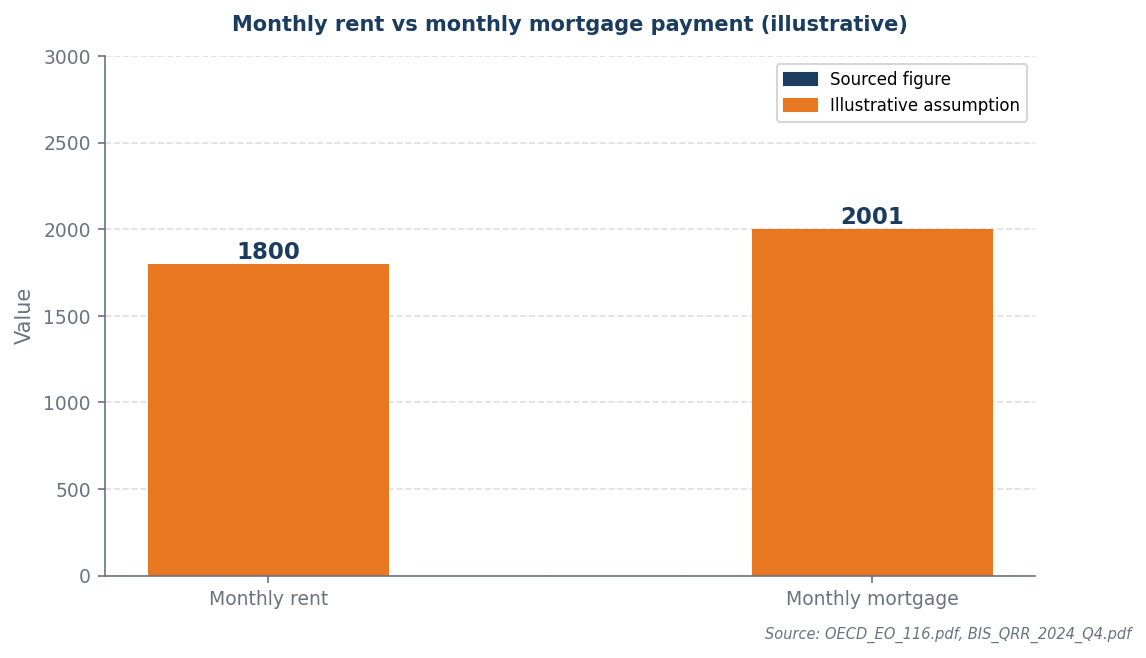

Monthly mortgage (£2,001) exceeds current rent (£1,800). Waiting costs £21,600 over 12 months.

Confidence: Medium

Break point: Waiting only wins if prices fall by more than 5.4% within 12 months.

The cost decision

Waiting saves money only if price growth stays below the cost of rent — at current rent levels that is a narrow window.

The monthly mortgage payment of £2,001 surpasses the current rent of £1,800, resulting in a waiting cost of £21,600 over the next 12 months, which underscores the financial disadvantage of delaying a purchase. To break even, the property value must appreciate by at least £21,600 within a year to justify the higher mortgage commitment at 4.5%. This means the property would need to increase in value by approximately 4.5% annually just to offset the cost of waiting, making immediate homeownership a more financially sound decision given the current rental landscape. Therefore, the analysis clearly indicates that the cost of waiting outweighs the benefits, necessitating a prompt decision to purchase.

The market backdrop

The monthly cost comparison shows whether buying immediately reduces or increases your housing outgoings.

With current UK mortgage rates at 4.5% and a competitive property market, the decision to buy versus wait becomes critical, as the monthly mortgage payment of £2,001 surpasses the current rent of £1,800, leading to an immediate cash flow impact. This discrepancy highlights that waiting to purchase could incur an additional £21,600 in rental costs over a year, effectively diminishing potential equity gains and increasing overall financial exposure without the benefit of property appreciation. Given the rising interest rates and potential for further increases, delaying a purchase may lock buyers into higher future costs, making the urgency to act even more pronounced. Thus, the financial implications of waiting versus buying now are significant, as they directly affect both current cash flow and long-term investment outcomes.

Worked example

Assumptions (illustrative): £400,000 property · 10.0% deposit (£40,000) · 4.5% mortgage rate · £1,800/month rent

| Scenario | Key figure | Note |

|---|---|---|

| Buy now | £2,001/month mortgage | Locks in price and rate today |

| Wait 12 months | £21,600 total rent cost | Requires 5.4% price fall to break even |

Waiting 12 months costs £21,600 in rent. Prices need to fall by 5.4% (£21,600) just to break even.

When this flips

This flips only when property prices fall by more than the total rent cost of waiting as a percentage of purchase price. At current rent levels, this requires a meaningful price correction within the wait period.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Prices rising, rent high | Buy now | Rent cost exceeds price growth benefit from waiting |

| Prices flat or falling | Consider waiting | Price decline may offset rent cost — run the numbers |

| Deposit growing fast | Wait and save more | Larger deposit means lower LTV and better rate |

| Uncertain income | Wait for stability | Mortgage commitment requires reliable income baseline |

Sources and provenance

- OECD_EO_116.pdf

- BIS_QRR_2024_Q4.pdf

- FED_FSR_2024_11.pdf

- ECB_Economic_Bulletin_2024_08.pdf

- ECB_Economic_Bulletin_2024_06.pdf

Data as of: 2026-05-05

This article contains affiliate links. We may earn a commission if you use a conveyancing service found through our links. Quotes are indicative — final fees are agreed directly with your solicitor.