ISA vs Pension: Which is Right for You?

Verdict

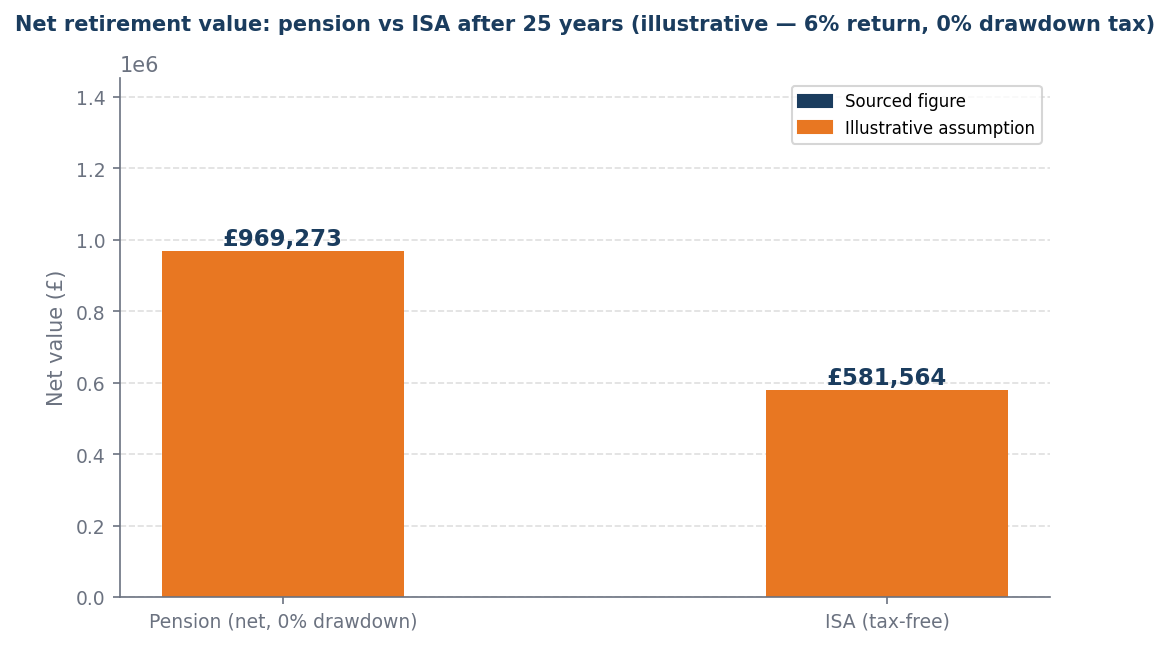

Pension wins by £387,709 net over 25 years. 40% relief on entry, 0% tax on drawdown.

Confidence: High

Break point: This flips if your drawdown tax rate rises above 40% — the point where pension tax advantage disappears.

The tax decision

Higher-rate taxpayers get 40p of relief for every £1 contributed — the ISA cannot match that on entry cost alone.

The pension option delivers a net gain of £387,709 over 25 years due to the significant 40% tax relief on contributions, which reduces the effective cost of investing today, compared to other investment vehicles that do not offer such relief. This upfront benefit allows for a larger capital base to grow tax-free, compounding over time, while the 0% tax on drawdown ensures that the entire accumulated value can be accessed without further taxation at retirement. Consequently, the net cost today is substantially lower than the net value realized at retirement, making the pension the superior financial choice.

Worked example

Worked example (illustrative): £10,000/yr net contribution. At 40% marginal rate, pension is grossed up to £16,667 (HMRC adds £6,667 relief). Over 25 years at 6% return: Pension net value (after 0% drawdown tax + 25% TFLS) = £969,273. ISA net value (tax-free) = £581,564. Verdict: Pension wins by £387,709.

When this flips

This flips only when your expected drawdown tax rate rises above 40.0% — the point where pension relief no longer compensates for drawdown tax. The ISA wins on flexibility if you need access before age 57 or your horizon is under 25 years.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Higher rate taxpayer now, basic rate at retirement | Maximise pension first | 40% relief in, 20% tax out — pension wins by the widest margin |

| Basic rate taxpayer at both ends | Pension still ahead, but ISA flexibility matters | Pension timing advantage is real but smaller — weigh access needs |

| Need access before age 57 | ISA for short-term, pension for long-term | Pension locked until 57 (2028) — split contributions if flexibility needed |

| Approaching retirement, expect higher drawdown rate | Shift contributions toward ISA | If drawdown rate will exceed your current marginal rate, pension advantage disappears |

Sources and provenance

Data as of: 2026-04-06