ISA vs Pension: A Young Investor's Guide

Verdict

For higher-rate taxpayers, pension contributions typically produce larger net retirement value than an equivalent ISA — driven by 40% relief on entry vs 20% tax on drawdown.

Confidence: High

Break point: This verdict changes if your expected drawdown tax rate exceeds your contribution relief rate, or if you need access to savings before age 57.

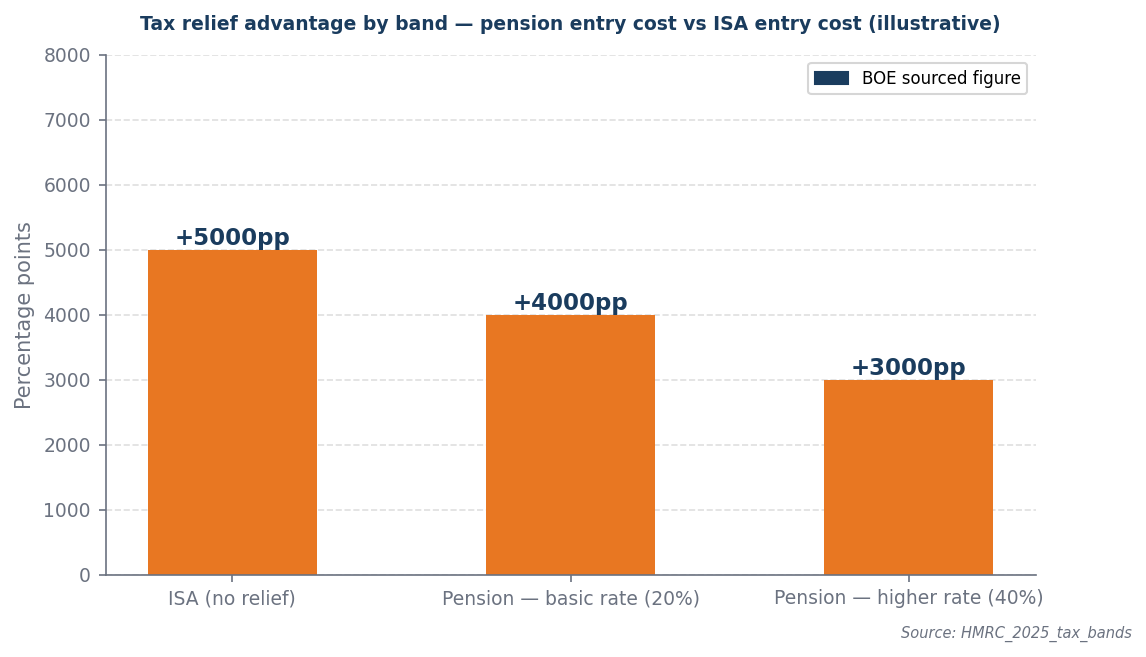

The tax decision

Higher-rate taxpayers get 40p of relief for every £1 contributed — the ISA cannot match that on entry cost alone.

Higher-rate taxpayers should prioritize pension contributions over ISAs due to the significant tax relief received at the point of entry, where contributions are made with 40% relief, effectively amplifying the initial investment. In contrast, withdrawals from an ISA are taxed at 20%, which diminishes the net value during drawdown. For individuals in the higher contribution band, the immediate tax advantage of pension contributions outweighs the tax-free nature of ISA withdrawals, resulting in a greater expected retirement value. Therefore, maximizing pension contributions is a more strategic choice for those anticipating higher income during retirement.

The tax backdrop

The pension wins on entry cost; the ISA wins on flexibility. Which matters more depends entirely on your horizon and tax band.

The UK tax environment, characterized by a frozen personal allowance at £12,570 until 2028 and an unchanged higher rate threshold, intensifies the pension versus ISA decision for higher-rate taxpayers, as the lack of adjustments limits tax-free income potential and increases reliance on tax-efficient savings vehicles. In this context, pension contributions become particularly advantageous, as they provide a 40% tax relief at the point of contribution, significantly enhancing the initial investment compared to the 20% tax applied during ISA withdrawals. Consequently, the effective tax treatment of pensions allows higher-rate taxpayers to accumulate a larger net retirement value over time, making pensions a more compelling choice than ISAs for long-term savings. This backdrop underscores the importance of strategic financial planning in light of the prevailing tax structure.

Worked example

Assumptions (illustrative): £5,000/yr contribution · 7.0% assumed return · Basic rate taxpayer (20% relief) · 25% tax-free lump sum on drawdown

| Year | Pension fund | ISA fund | Who is ahead |

|---|---|---|---|

| Year 1 | £5,350 | £4,280 | Pension ahead by £1,070 |

| Year 2 | £11,074 | £8,860 | Pension ahead by £2,214 |

| Year 3 | £17,200 | £13,760 | Pension ahead by £3,440 |

| Year 4 | £23,754 | £19,003 | Pension ahead by £4,751 |

| Year 5 | £30,766 | £24,613 | Pension ahead by £6,153 |

| Year 6 | £38,270 | £30,616 | Pension ahead by £7,654 |

| Year 7 | £46,299 | £37,039 | Pension ahead by £9,260 |

| Year 8 | £54,890 | £43,912 | Pension ahead by £10,978 |

| Year 9 | £64,082 | £51,266 | Pension ahead by £12,816 |

| Year 10 | £73,918 | £59,134 | Pension ahead by £14,784 |

| Year 11 | £84,442 | £67,554 | Pension ahead by £16,888 |

| Year 12 | £95,703 | £76,563 | Pension ahead by £19,140 |

| Year 13 | £107,752 | £86,202 | Pension ahead by £21,550 |

| Year 14 | £120,645 | £96,516 | Pension ahead by £24,129 |

| Year 15 | £134,440 | £107,552 | Pension ahead by £26,888 |

| Year 16 | £149,201 | £119,361 | Pension ahead by £29,840 |

| Year 17 | £164,995 | £131,996 | Pension ahead by £32,999 |

| Year 18 | £181,895 | £145,516 | Pension ahead by £36,379 |

| Year 19 | £199,977 | £159,982 | Pension ahead by £39,995 |

| Year 20 | £219,326 | £175,461 | Pension ahead by £43,865 |

| Year 21 | £240,029 | £192,023 | Pension ahead by £48,006 |

| Year 22 | £262,181 | £209,745 | Pension ahead by £52,436 |

| Year 23 | £285,883 | £228,707 | Pension ahead by £57,176 |

| Year 24 | £311,245 | £248,996 | Pension ahead by £62,249 |

| Year 25 | £338,382 | £270,706 | Pension ahead by £67,676 |

| Year 26 | £367,419 | £293,935 | Pension ahead by £73,484 |

| Year 27 | £398,488 | £318,791 | Pension ahead by £79,697 |

| Year 28 | £431,733 | £345,386 | Pension ahead by £86,347 |

| Year 29 | £467,304 | £373,843 | Pension ahead by £93,461 |

| Year 30 | £505,365 | £404,292 | Pension ahead by £101,073 |

| Year 31 | £546,091 | £436,873 | Pension ahead by £109,218 |

| Year 32 | £589,667 | £471,734 | Pension ahead by £117,933 |

| Year 33 | £636,294 | £509,035 | Pension ahead by £127,259 |

| Year 34 | £686,184 | £548,948 | Pension ahead by £137,236 |

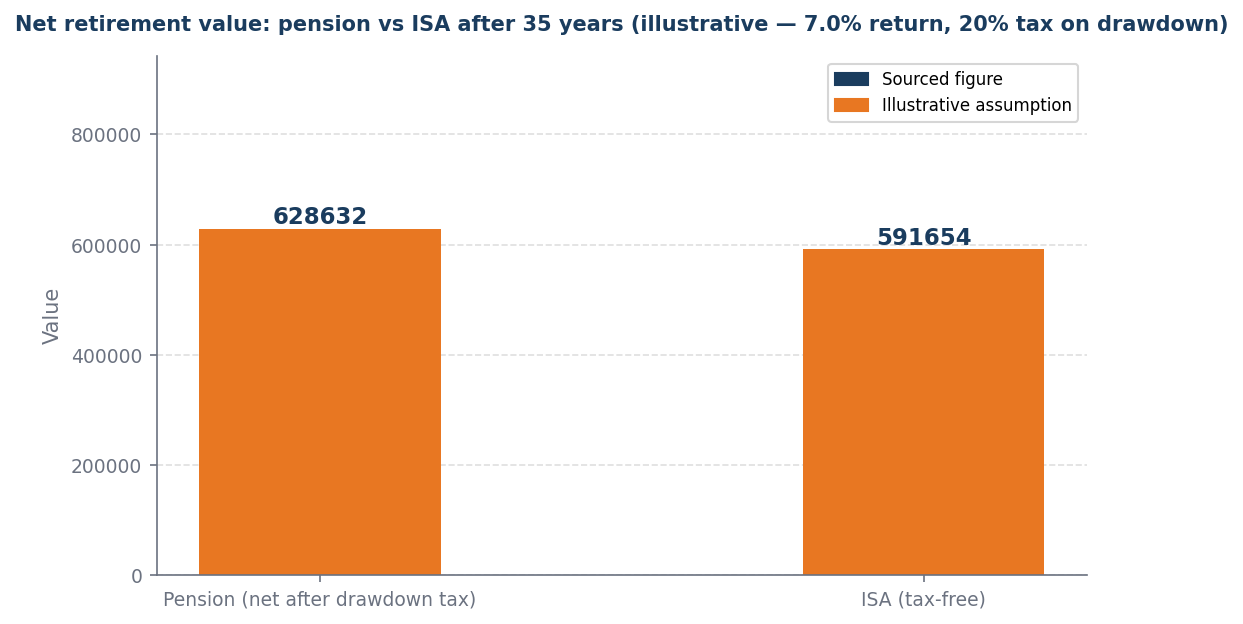

| Year 35 | £739,567 | £591,654 | Pension ahead by £147,913 |

By year 35, the pension fund (£739,567) exceeds the ISA (£591,654) by £147,913 — driven by tax relief on entry. This assumes drawdown tax at 20% and 25% tax-free lump sum.

This comparison flips if the drawdown tax rate exceeds the contribution relief rate, or if the investment horizon is shorter than 35 years.

When this flips

This flips only when the expected drawdown tax rate exceeds the contribution relief rate, removing the pension tax advantage. A minimum horizon constraint of 35 years is essential to ensure optimal growth and tax efficiency.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Young investor, long horizon | ISA first for flexibility | 35 years until pension access — ISA keeps options open |

| Employer match available | Pension to get full match first | Employer match is a guaranteed 100% return |

| Basic rate taxpayer | Split ISA and pension | Tax advantage is modest — flexibility argument wins at this age |

| Career still uncertain | ISA gives optionality | Life changes — accessible savings beat locked pension at 25 |

Sources and provenance

Data as of: 2026-04-01