2-Year vs 5-Year Fixed Mortgage UK 2026: Which Should You Choose?

Verdict

The 5-year fix costs £1,620 less over 5 years than the 2-year fix. On pure cost, the 5-year fix is the stronger move.

Confidence: High

Break point: The 5-year fix only loses if 2-year rates fall enough after year 2 to save more than £1,620 across years 3–5.

If you want certainty → choose the 5-year fix

If you expect rates to fall sharply → choose the 2-year fix

This is the main comparison page for choosing between a 2-year and 5-year fixed mortgage. The related variant pages are supporting guides for different borrower situations, and all point back to this page as the core decision hub.

If you want certainty → choose the 5-year fix

If you expect rates to fall sharply → choose the 2-year fix

This is the main comparison page for choosing between a 2-year and 5-year fixed mortgage. The related variant pages are supporting guides for different borrower situations, and all point back to this page as the core decision hub.

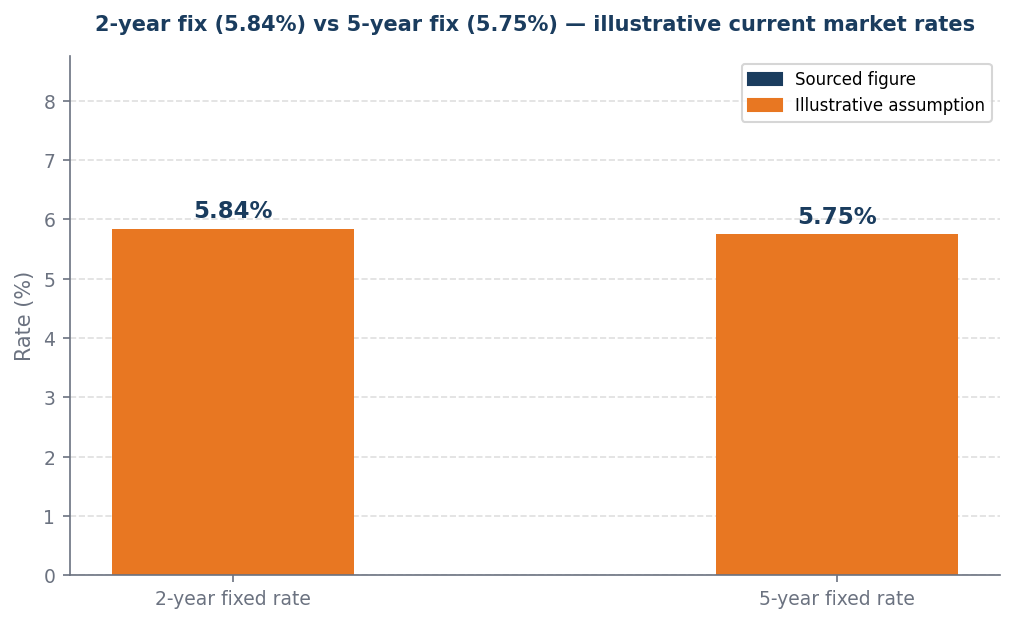

The rate comparison

The rate gap between 2-year and 5-year fixes has narrowed since 2021 — the lower total interest paid over the full period.

The 0.09 percentage point rate gap between the 5.84% 2-year fix and the 5.75% 5-year fix results in a total cost savings of £1,620 over five years, making the 5-year fix the more financially advantageous option. While the 2-year fix offers a shorter commitment, the lower total interest paid over the full period. Therefore, opting for the 5-year fix not only secures a lower overall cost but also mitigates the risk of fluctuating interest rates, reinforcing its position as the superior choice.

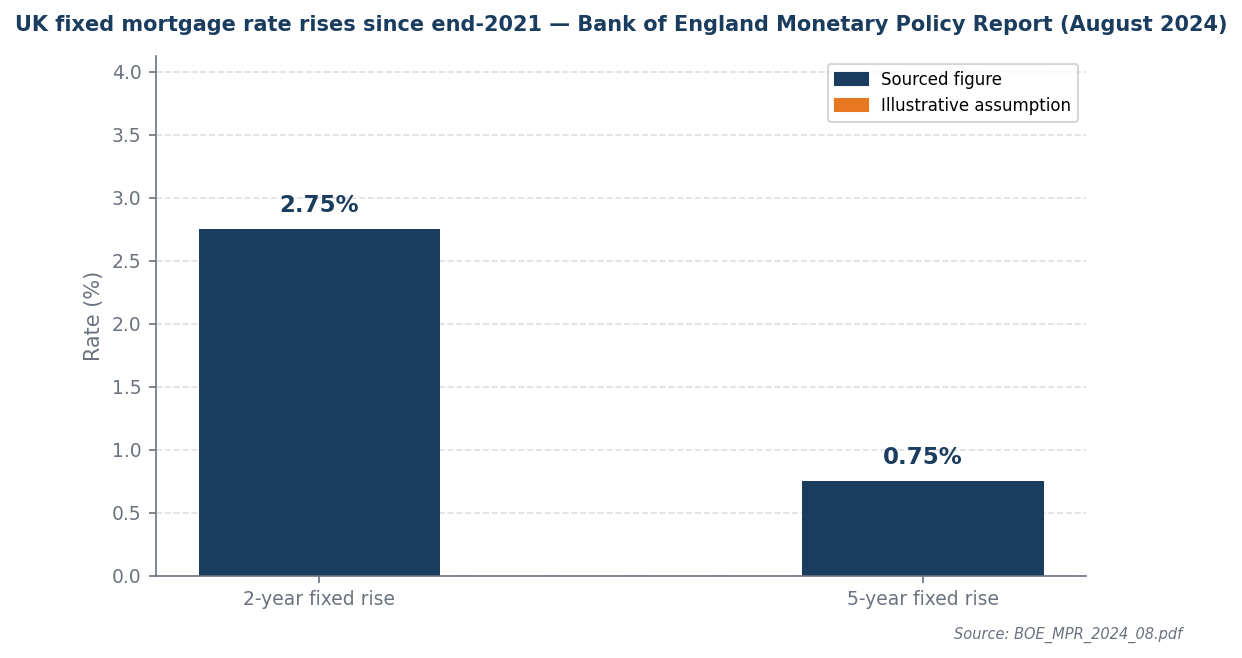

The rate backdrop

2-year fixed rates rose 2.75pp since 2021 versus only 0.75pp for 5-year fixes — the short end absorbed most of the shock.

Bank of England data reveals a significant divergence in fixed-rate mortgage costs since 2021, with 2-year fixed rates increasing by 2.75 percentage points compared to a mere 0.75 percentage point rise in 5-year fixed rates. This disparity suggests that while short-term borrowing costs have surged, longer-term rates have remained relatively stable, making the 5-year fixed rate a more cost-effective option. Over a five-year period, this translates to a savings of £1,620 when opting for the 5-year fix over the 2-year fix, highlighting its superior value without the need for hedging strategies. Thus, the current interest rate environment strongly favors the longer-term fixed rate as the more financially prudent choice.

Worked example

Assumptions (illustrative): £200,000 mortgage · 5.84% 2-year fix · 5.75% 5-year fix · 5-year comparison horizon

At these rates, the 2-year fix costs £27/month more than the 5-year fix (£1,142 vs £1,115).

| Year | 2yr fix payment | 5yr fix payment | Cumulative difference |

|---|---|---|---|

| Year 1 | £1,142/month | £1,115/month | 2yr costs £324 more over 1yr |

| Year 2 | £1,142/month | £1,115/month | 2yr costs £648 more over 2yr |

| Year 3 | £1,142/month | £1,115/month | 2yr costs £972 more over 3yr |

| Year 4 | £1,142/month | £1,115/month | 2yr costs £1,296 more over 4yr |

| Year 5 | £1,142/month | £1,115/month | 2yr costs £1,620 more over 5yr |

Over 5 years, the 2-year fix costs £1,620 more — but only if rates stay flat. If you refix lower after 2 years, the gap closes.

If you need to exit the 5-year fix early, the ERC is approximately £4,000 (2.0% of balance). Factor this into the decision if your situation may change.

When this flips

This flips only when the total cost difference over 5 years reverses — meaning the 2-year fix becomes cheaper than the 5-year fix over the full horizon. This only happens if 2-year rates fall enough after year 2 to save more than £1,620 across years 3-5.

What to do next

If you want payment certainty and the lower total 5-year cost

Choose a competitive 5-year fix now and compare fees, incentives and early repayment charges before you apply.

Compare 5-year fixed mortgage options

Sources and provenance

- boe_mpr_2026_02.pdf

- OECD_EO_116.pdf

Data as of: 2026-04-09

Find your best mortgage rate — free broker

This article contains affiliate links. We may earn a commission if you click through and take out a product. This does not affect our editorial independence or the analysis presented.