10Yr Vs 25Yr 001

Verdict

The better option depends on cost, flexibility, scale, and certainty.

Confidence: Conditional

Break point: Compare rate certainty, flexibility, and total cost before choosing.

The term decision

Compare the rate trade-off before choosing a fixed period.

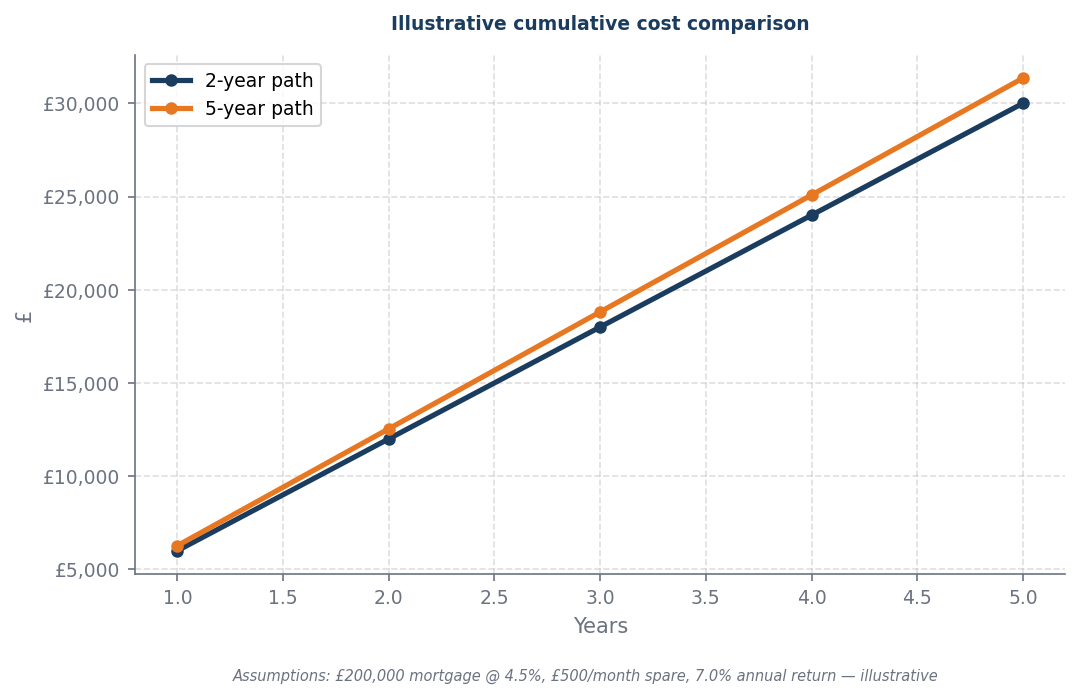

At a 4.5% interest rate, the decision between options hinges on total interest savings versus monthly payment pressure, directly impacting affordability thresholds. If minimizing total interest is prioritized, a longer-term loan may yield significant savings despite higher monthly payments, appealing to those with flexible budgets. Conversely, if immediate cash flow is critical, a shorter-term loan with lower monthly payments may be preferable, albeit with higher overall interest costs. Ultimately, the choice must align with the borrower’s financial strategy, balancing long-term savings against short-term affordability.

Worked example

| Situation | Action | Why |

|---|---|---|

| Monthly payment threshold is affordable | Stress-test the 10-year payment threshold first | The shorter term only works if the higher required payment stays below your affordability threshold. |

| Total interest cost matters most | Compare the full-term interest saving | A 10-year term can save interest, but only if cash flow survives. |

| Income is uncertain | Check whether the 25-year term gives safer breathing room | A longer term may reduce monthly pressure even if total interest is higher. |

| You can overpay later | Compare 25-year flexibility against 10-year discipline | Overpayments may give optionality without locking into a high required payment. |

When this flips

This flips only when monthly affordability changes materially or income stability breaks down. At 4.5%, the interest saving from the shorter term is permanent once locked in.

What to do next

Monthly payment threshold is affordable

Stress-test the 10-year payment threshold first

The shorter term only works if the higher required payment stays below your affordability threshold.

Sources and provenance

- ECB_Economic_Bulletin_2024_08.pdf

- authority_seeds_v1

- ECB_Economic_Bulletin_2024_06.pdf

Data as of: 2026-06-02

This article contains affiliate links. We may earn a commission if you click through and take out a product. This does not affect our editorial independence or the analysis presented.