Refinance Vs Stay On Your Mortgage In 2026

Verdict

The better option depends on cost, flexibility, scale, and certainty.

Confidence: Conditional

Break point: Compare rate certainty, flexibility, and total cost before choosing.

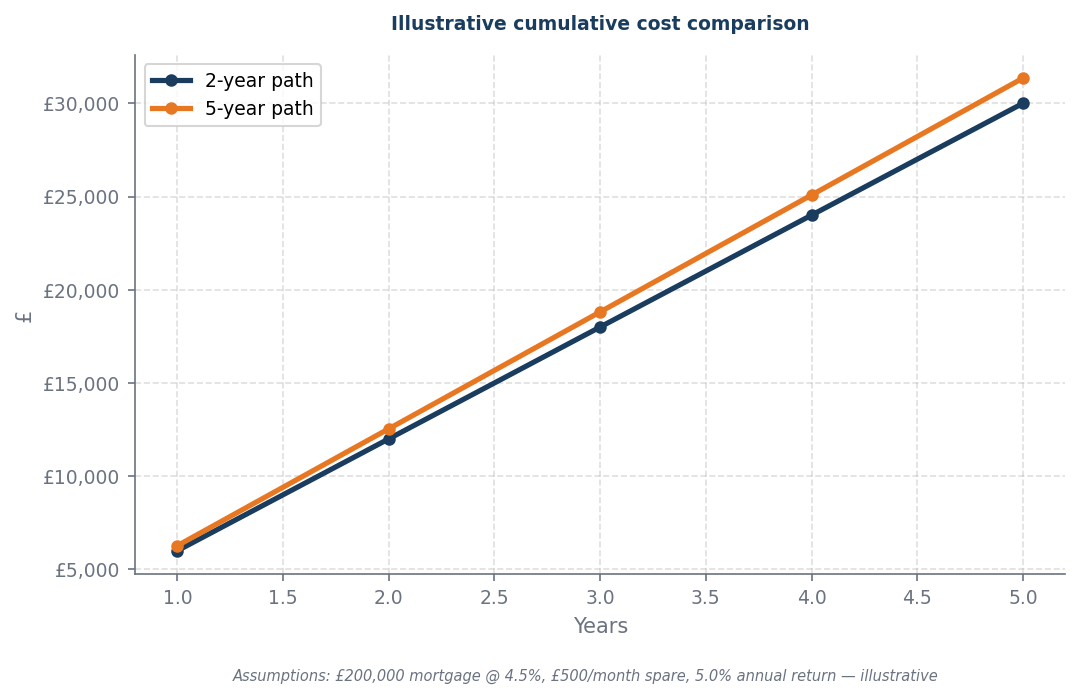

The refinance saving

Compare the rate trade-off before choosing a fixed period.

When considering refinancing, it's crucial to ensure that the new mortgage deal effectively reduces your total cost after accounting for all associated fees, early repayment charges, and the time it takes to break even on the new arrangement. If the lower interest rate does not sufficiently offset these costs, refinancing may not be the better option. Additionally, assess the flexibility of the new mortgage terms, as a more adaptable deal could provide significant long-term benefits. Scale is also important; larger loans may yield different savings than smaller ones, impacting the overall decision. Certainty in your financial situation and future interest rate trends should guide your choice, as a stable environment may favour sticking with your current mortgage. Ultimately, the decision hinges on a thorough analysis of these factors to determine the most cost-effective path forward.

Worked example

| Situation | Action | Why |

|---|---|---|

| New deal is materially cheaper | Run the break-even calculation first | A lower rate only matters if the saving clears fees and charges. |

| Fees or early repayment charges are high | Stress-test staying put | Costs can erase the benefit of refinancing. |

| You may move or refinance again soon | Compare the holding period | Short horizons make break-even harder. |

| Payment certainty matters | Compare total monthly resilience | The best answer is the one your budget can sustain. |

Refinance Vs Stay On Your Mortgage In 2026

When this flips

This flips only when the rate saving, fees, early repayment charges, or expected holding period change materially. Refinancing is only worth it when the monthly saving survives the full break-even test.

What to do next

| Your situation | Action | Why |

|---|---|---|

| New deal is materially cheaper | Run the break-even calculation first | A lower rate only matters if the saving clears fees and charges. |

| You may move or refinance again soon | Compare the holding period | Short horizons make break-even harder. |

Sources and provenance

- OECD_EO_116.pdf

- ECB_Economic_Bulletin_2024_06.pdf

- authority_seeds_v1

- fg23-2.txt

Data as of: 2026-06-02

This article contains affiliate links. We may earn a commission if you click through and take out a product. This does not affect our editorial independence or the analysis presented.