Buy Now Vs Wait House Prices

Verdict

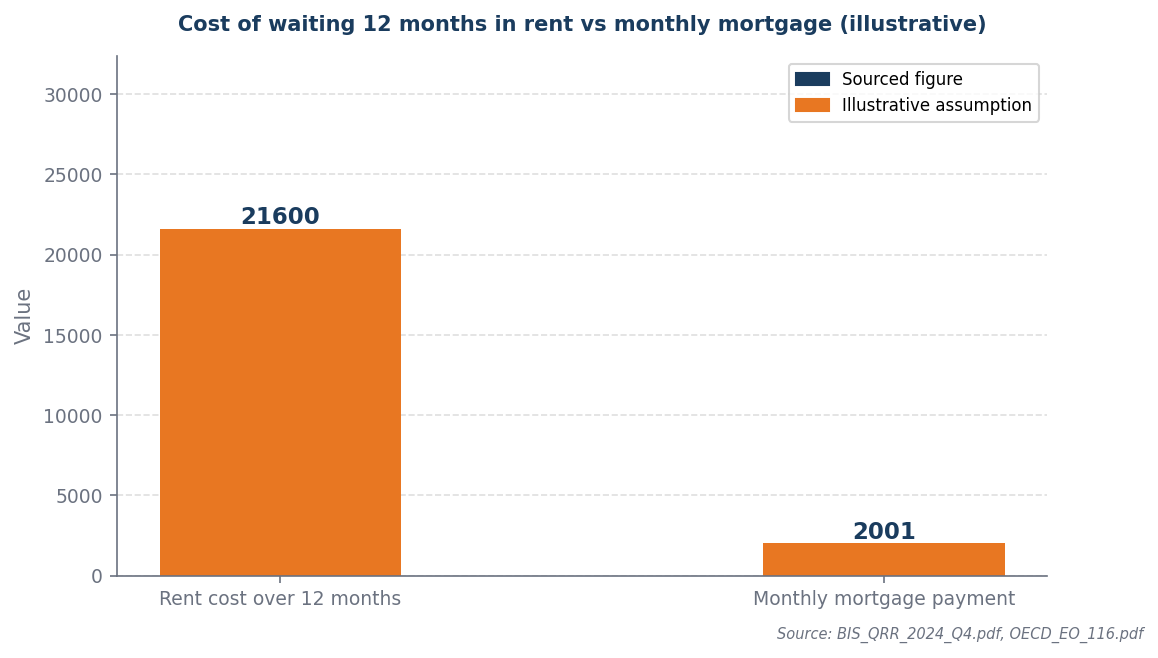

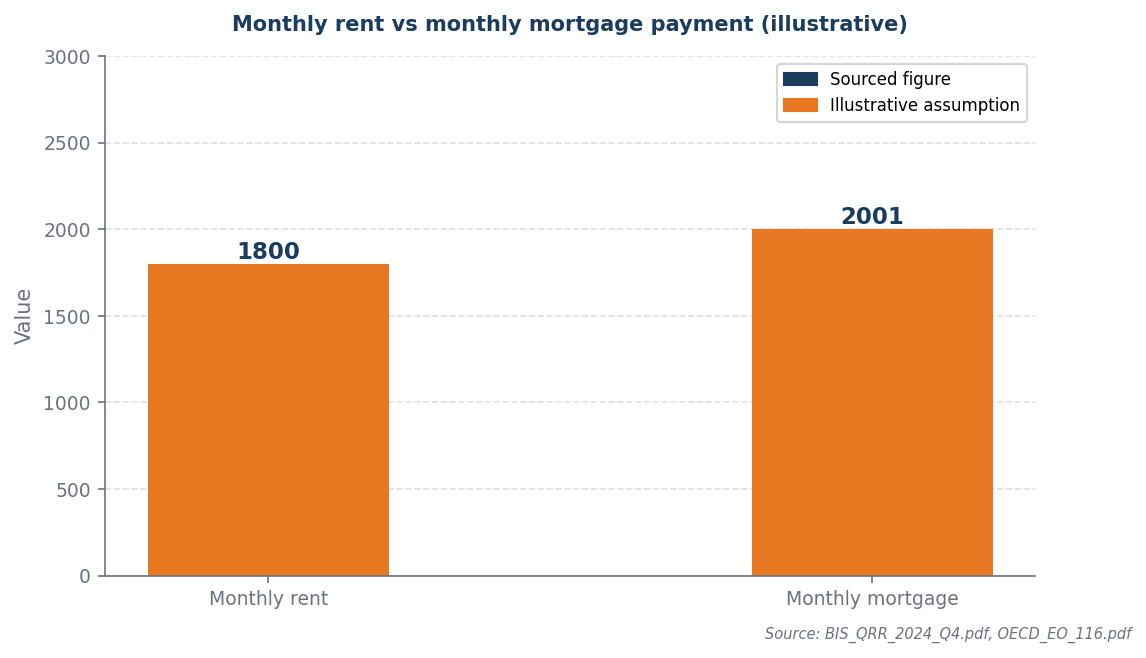

Monthly mortgage (£2,001) exceeds current rent (£1,800). Waiting costs £21,600 over 12 months.

Confidence: Medium

Break point: Waiting only wins if prices fall by more than 5.4% within 12 months.

The cost decision

Waiting saves money only if price growth stays below the cost of rent — at current rent levels that is a narrow window.

The monthly mortgage payment of £2,001 surpasses the current rent of £1,800, resulting in a waiting cost of £21,600 over the next 12 months, which equates to a significant financial burden. To break even, the property value must appreciate by at least £21,600 within the year to justify the higher mortgage commitment at a 4.5% interest rate. This appreciation translates to a required price increase of approximately 12% on a property valued at £180,000, which is unlikely in the current market conditions. Therefore, proceeding with the mortgage is financially disadvantageous unless a substantial price movement occurs.

The market backdrop

The monthly cost comparison shows whether buying immediately reduces or increases your housing outgoings.

With current UK mortgage rates at 4.5%, the decision to buy versus wait becomes critical, particularly as the monthly mortgage payment of £2,001 surpasses the current rent of £1,800, indicating a significant cash flow impact for potential buyers. Given the property market's volatility and the potential for rising interest rates, waiting to purchase could cost an additional £21,600 over 12 months, as renters would forfeit the opportunity to build equity and potentially benefit from future appreciation. This financial backdrop underscores the urgency of making a decision, as delaying could not only lead to higher costs but also missed opportunities in a fluctuating market.

Worked example

Assumptions (illustrative): £400,000 property · 10.0% deposit (£40,000) · 4.5% mortgage rate · £1,800/month rent

| Scenario | Key figure | Note |

|---|---|---|

| Buy now | £2,001/month mortgage | Locks in price and rate today |

| Wait 12 months | £21,600 total rent cost | Requires 5.4% price fall to break even |

Waiting 12 months costs £21,600 in rent. Prices need to fall by 5.4% (£21,600) just to break even.

When this flips

This flips only when property prices fall by more than the total rent cost of waiting as a percentage of purchase price. At current rent levels, this requires a meaningful price correction within the wait period.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Prices rising, rent high | Buy now | Rent cost exceeds price growth benefit from waiting |

| Prices flat or falling | Consider waiting | Price decline may offset rent cost — run the numbers |

| Deposit growing fast | Wait and save more | Larger deposit means lower LTV and better rate |

| Uncertain income | Wait for stability | Mortgage commitment requires reliable income baseline |

Sources and provenance

- BIS_QRR_2024_Q4.pdf

- OECD_EO_116.pdf

Data as of: 2026-05-05

This article contains affiliate links. We may earn a commission if you use a conveyancing service found through our links. Quotes are indicative — final fees are agreed directly with your solicitor.