10-Year vs 25-Year Mortgage: Which is Right for You?

Verdict

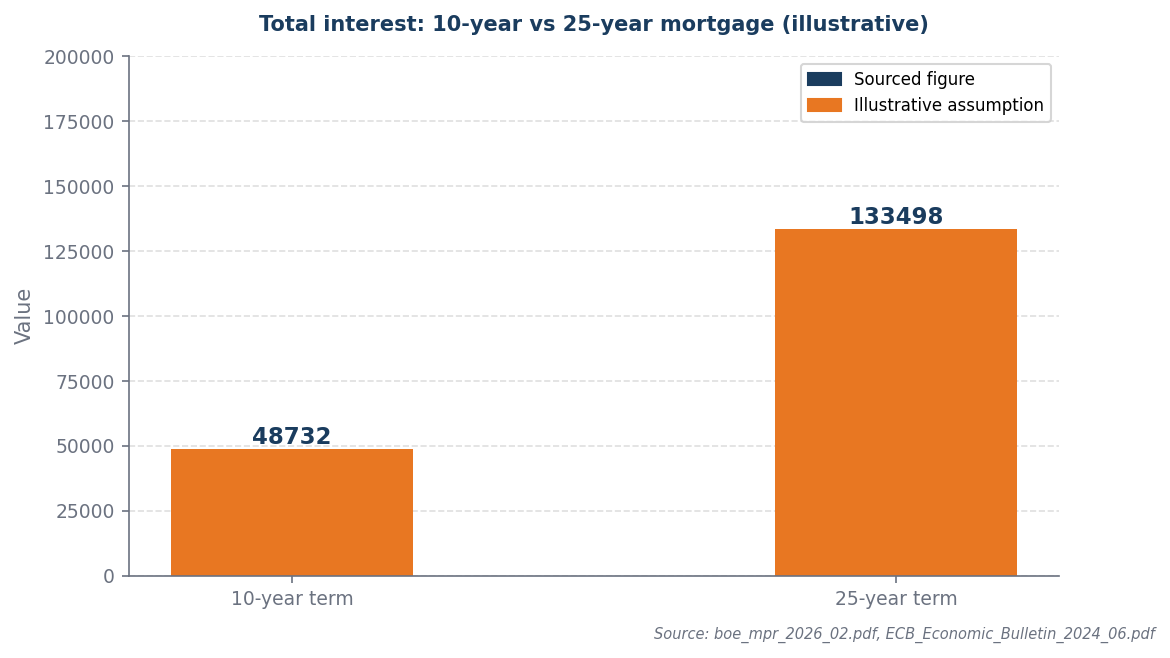

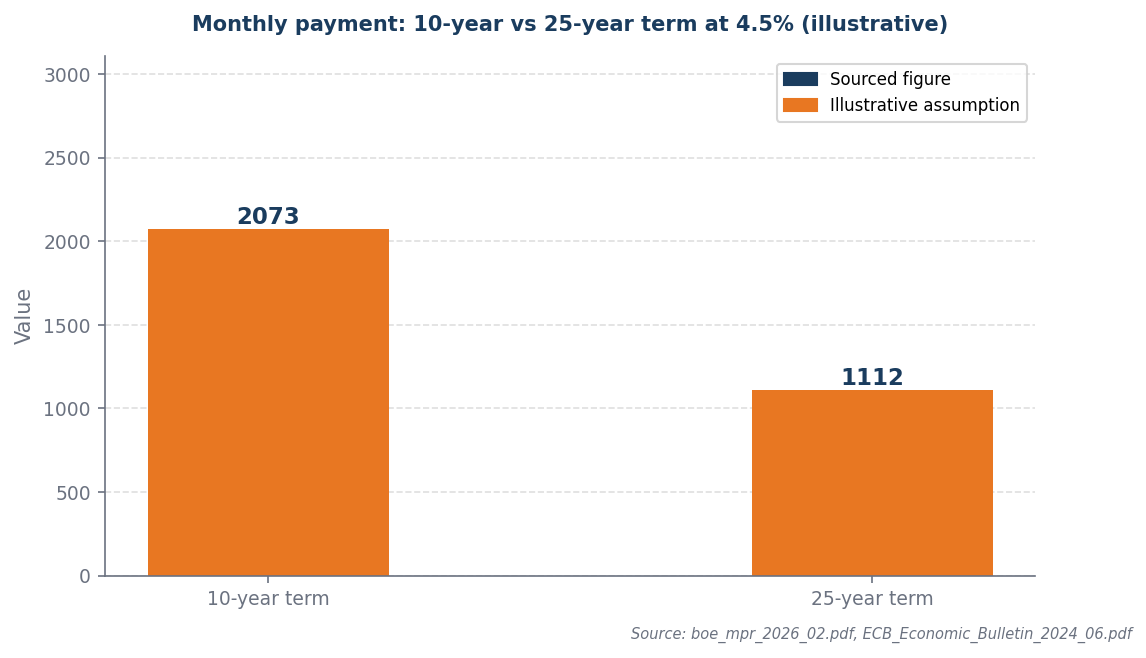

A 10-year term saves £84,767 in total interest vs 25 years, but costs £961 more per month.

Confidence: High

Break point: The 10-year term only makes sense if you can comfortably afford £2,073/month.

The term decision

The 10-year term saves significantly in total interest — but only if the higher monthly payment is genuinely affordable.

Choosing a 10-year term at 4.5% saves £84,767 in total interest compared to a 25-year term, but increases monthly payments by £961, which may exceed your affordability threshold. This significant interest saving is compelling for those who can comfortably manage the higher monthly outlay, as it reduces long-term financial burden. However, if the increased monthly payment strains your budget, the 25-year option, despite its higher total interest cost, may be the more prudent choice to maintain financial stability. Prioritize your cash flow and ensure that your monthly obligations align with your overall financial strategy.

The interest cost

The monthly payment gap is the real constraint — total interest saving only matters if the higher payment is affordable.

With mortgage rates at 4.5%, the choice of term length becomes a pivotal financial decision, as higher rates significantly increase the total interest paid over the life of the loan. For instance, opting for a 10-year term can save £84,767 in total interest compared to a 25-year term, highlighting the substantial long-term savings achievable despite the higher monthly payment of £961. This stark contrast underscores the importance of balancing immediate cash flow with long-term financial benefits, as the elevated interest costs associated with longer terms can erode overall savings. Therefore, in a high-rate environment, shorter terms may offer a more favorable financial trajectory despite their initial affordability challenges.

Worked example

Assumptions (illustrative): £200,000 mortgage at 4.5%

| Term | Monthly payment | Total interest | Total cost |

|---|---|---|---|

| 10-year term | £2,073 | £48,732 | £248,732 |

| 25-year term | £1,112 | £133,498 | £333,498 |

The 10-year term saves £84,766 in total interest but costs £961 more per month. That is the trade-off.

When this flips

This flips only when monthly affordability changes materially or income stability breaks down. At 4.5%, the interest saving from the shorter term is permanent once locked in.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Want flexibility with discipline | 25yr + overpay to 10yr rate | Same payoff timeline, lower contractual floor |

| Income drops unexpectedly | Drop to minimum 25yr payment | Overpay strategy gives a floor to fall back on |

| Rate rises sharply | Reduce overpayment amount | Adjust overpay level to match new affordability |

| Lump sum available | Redirect lump sum to balance | One-off reduction accelerates crossover point |

Sources and provenance

- boe_mpr_2026_02.pdf

- ECB_Economic_Bulletin_2024_06.pdf

Data as of: 2026-04-01