10-Year vs 25-Year Mortgage: The True Cost Difference

Verdict

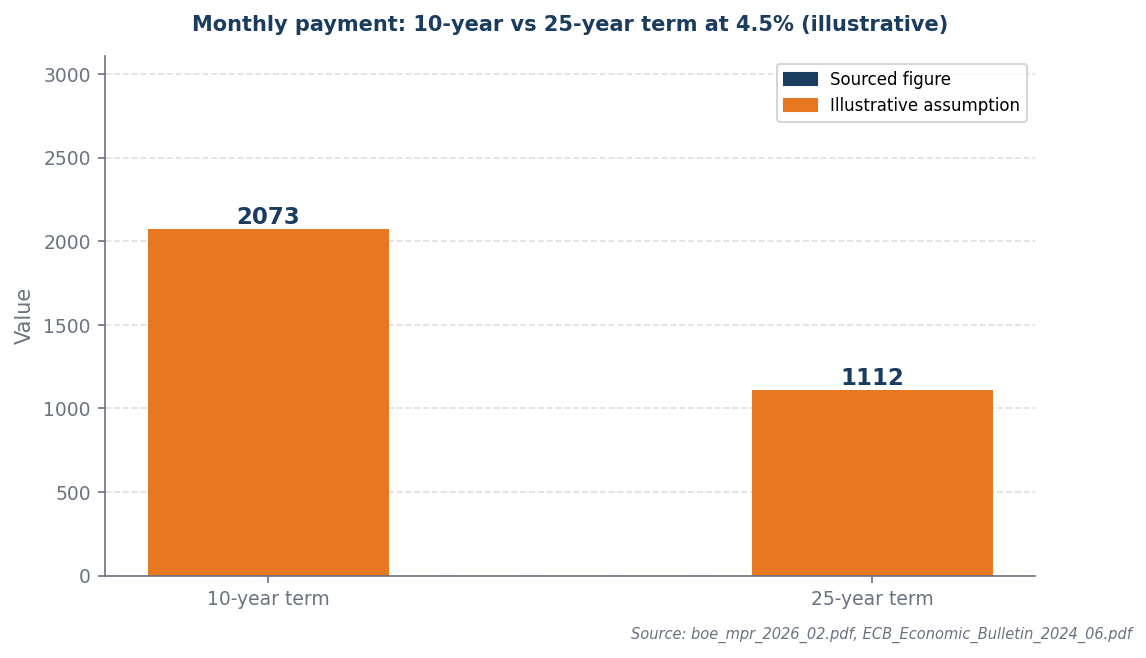

A 10-year term saves £84,767 in total interest vs 25 years, but costs £961 more per month.

Confidence: High

Break point: The 10-year term only makes sense if you can comfortably afford £2,073/month.

The term decision

The 10-year term saves significantly in total interest — but only if the higher monthly payment is genuinely affordable.

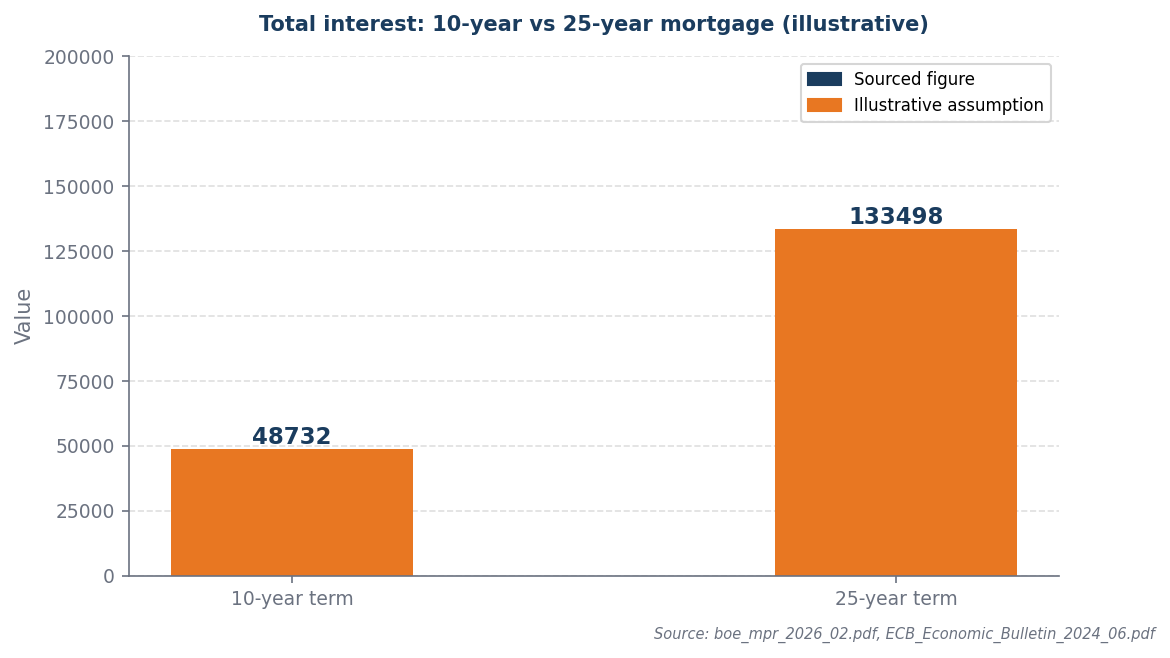

Choosing a 10-year term at 4.5% interest saves £84,767 in total interest compared to a 25-year term, making it a financially sound decision for those who can afford the higher monthly payment of £961. This significant interest saving underscores the long-term benefits of a shorter loan duration, which outweighs the immediate cash flow pressure. However, the affordability threshold must be carefully considered; if the increased monthly payment stretches your budget too thin, the long-term savings may not justify the short-term strain. Ultimately, for financially stable borrowers, the 10-year option is the clear choice for maximizing savings.

The interest cost

The monthly payment gap is the real constraint — total interest saving only matters if the higher payment is affordable.

With mortgage rates at 4.5%, the cost of borrowing becomes significantly more pronounced, making the choice of term length a pivotal financial decision. A 10-year term, while resulting in higher monthly payments of £961 more than a 25-year term, ultimately saves borrowers £84,767 in total interest over the life of the loan due to the accelerated repayment of principal and reduced interest accumulation. This stark contrast highlights how higher rates amplify the financial impact of term length, as the longer duration allows interest to compound more extensively, leading to substantially higher overall costs. Thus, in a high-rate environment, opting for a shorter term can yield significant long-term savings despite the immediate cash flow burden.

Worked example

Assumptions (illustrative): £200,000 mortgage at 4.5%

| Term | Monthly payment | Total interest | Total cost |

|---|---|---|---|

| 10-year term | £2,073 | £48,732 | £248,732 |

| 25-year term | £1,112 | £133,498 | £333,498 |

The 10-year term saves £84,766 in total interest but costs £961 more per month. That is the trade-off.

When this flips

This flips only when monthly affordability changes materially or income stability breaks down. At 4.5%, the interest saving from the shorter term is permanent once locked in.

What to do next

| Your situation | Action | Why |

|---|---|---|

| High income, stable cashflow | Take 10yr term | Save £80k+ in interest — if you can afford the payment |

| Stretched affordability | Take 25yr, overpay monthly | Lower floor payment gives safety net while accelerating payoff |

| Income uncertain | Take 25yr term | Flexibility is worth more than interest saving when income is variable |

| Near retirement | Take shorter term | Clear the mortgage before retirement income drops |

Sources and provenance

- boe_mpr_2026_02.pdf

- ECB_Economic_Bulletin_2024_06.pdf

Data as of: 2026-04-01