2-Year vs 5-Year Fixed Mortgage: Should You Lock In Now or Wait?

Verdict

With only a 0.20pp rate gap, the 5-year fix is the stronger move — the certainty premium is worth more than the marginal saving on the 2-year.

Confidence: Medium

Break point: This verdict holds while the rate gap stays below 0.75pp. If the gap widens above 0.75pp, the 2-year cost case becomes compelling.

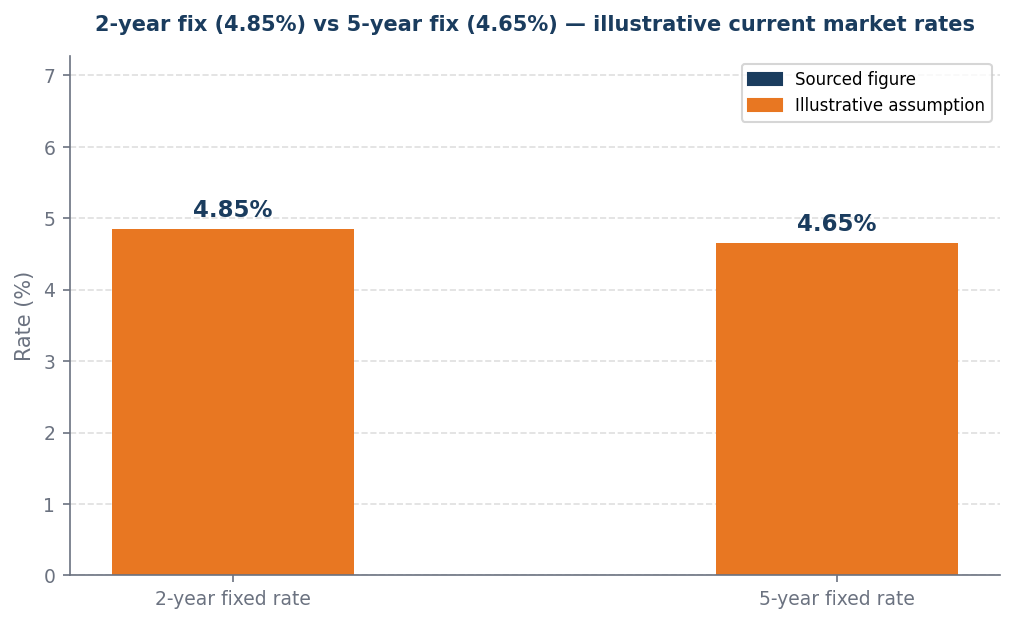

The rate comparison

The rate gap between 2-year and 5-year fixes has narrowed since 2021 — the certainty premium on the 5-year is historically low.

The 0.20 percentage point rate gap between the 4.85% 2-year fixed rate and the 4.65% 5-year fixed rate clearly favors the longer-term option, as the certainty premium associated with locking in a lower rate for five years outweighs the marginal savings of the shorter term. While the 2-year fix offers a slightly lower rate, the potential for rate increases in the near future poses a significant risk that could negate any short-term savings. The 5-year fix provides stability and predictability in budgeting, making it the more prudent choice for those prioritizing financial security over minimal cost savings. Therefore, opting for the 5-year fix is the superior decision in this scenario.

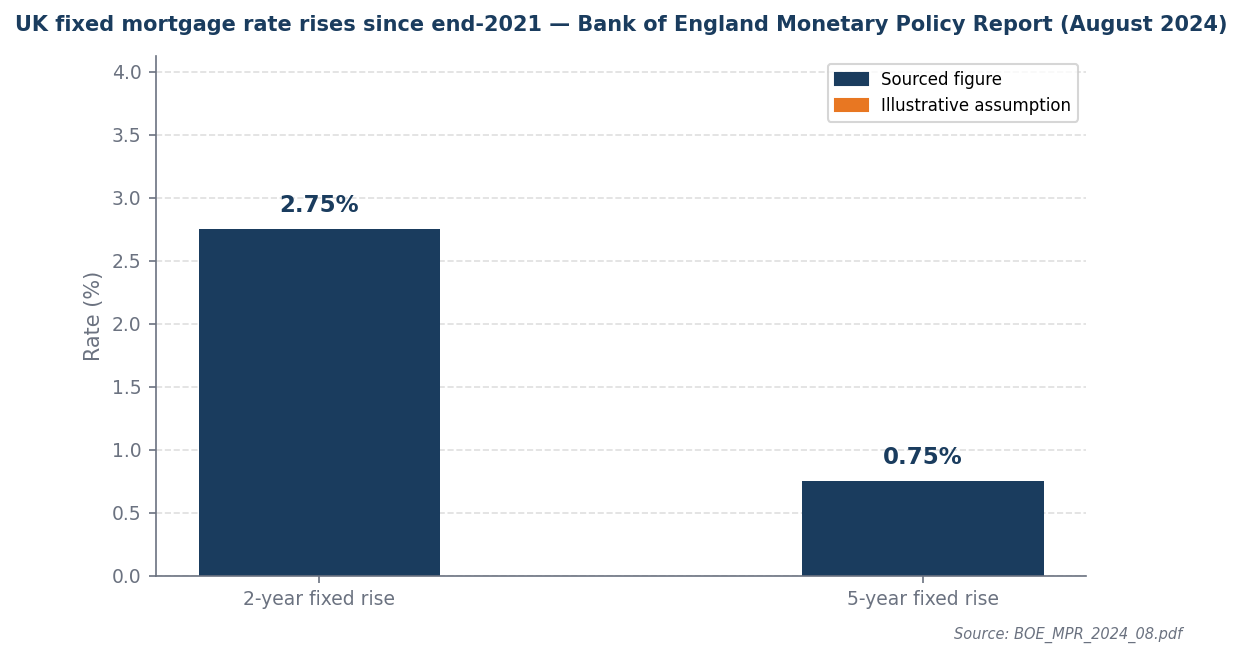

The rate backdrop

2-year fixed rates rose 2.75pp since 2021 versus only 0.75pp for 5-year fixes — the short end absorbed most of the shock.

Bank of England data indicates a significant divergence in fixed-rate mortgage trends since 2021, with 2-year fixed rates increasing by 2.75 percentage points compared to a mere 0.75 percentage point rise in 5-year fixed rates. This backdrop suggests that the minimal 0.20 percentage point gap between the two rates makes the 5-year fixed option more attractive, as it offers greater stability and predictability in an uncertain economic environment. The certainty premium associated with locking in a longer-term rate outweighs the marginal savings that a shorter-term 2-year fix might provide, making the 5-year fix a strategically sound choice for borrowers seeking to mitigate interest rate risk.

Worked example

Assumptions (illustrative): £200,000 mortgage · 4.85% 2-year fix · 4.65% 5-year fix · 5-year comparison horizon

At these rates, the 2-year fix costs £23/month more than the 5-year fix (£1,142 vs £1,119).

| Year | 2yr fix payment | 5yr fix payment | Cumulative difference |

|---|---|---|---|

| Year 1 | £1,142/month | £1,119/month | 2yr costs £276 more over 1yr |

| Year 2 | £1,142/month | £1,119/month | 2yr costs £552 more over 2yr |

| Year 3 | £1,142/month | £1,119/month | 2yr costs £828 more over 3yr |

| Year 4 | £1,142/month | £1,119/month | 2yr costs £1,104 more over 4yr |

| Year 5 | £1,142/month | £1,119/month | 2yr costs £1,380 more over 5yr |

Over 5 years, the 2-year fix costs £1,380 more — but only if rates stay flat. If you refix lower after 2 years, the gap closes.

If you need to exit the 5-year fix early, the ERC is approximately £4,000 (2.0% of balance). Factor this into the decision if your situation may change.

When this flips

This flips only when the rate gap between 2-year and 5-year fixes exceeds 0.75pp consistently. Below this threshold, the 5-year certainty premium wins.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Fixed income and you cannot absorb payment increases | Take the 5-year fix | Payment certainty for 5 years is worth more than a £23/month saving |

| Rate gap is small and your situation is stable | Take the 5-year fix | Two refix events in 5 years introduce unnecessary cost and admin risk |

| You may need to sell or remortgage early | Negotiate ERC terms before committing | ERC at 2% on £200k is £4,000 — check the exit cost before locking in |

| Uncertain about your situation in 2 years | Take the 5-year fix | Uncertainty is itself a reason to lock in — remove the refix decision entirely |

Sources and provenance

- boe_mpr_2026_02.pdf

- OECD_EO_116.pdf

Data as of: 2026-04-08

Find your best mortgage rate — free broker

This article contains affiliate links. We may earn a commission if you click through and take out a product. This does not affect our editorial independence or the analysis presented.