2-Year vs 5-Year Fixed Mortgage: What Rising Rates Mean for Your Decision

Verdict

With a 0.75pp rate gap, the 2-year fix is the stronger move — the cost saving is material enough to justify two refixing events.

Confidence: Conditional

Break point: This verdict holds while the rate gap stays at or above 0.5pp. If the gap narrows below 0.5pp, the 5-year certainty argument strengthens.

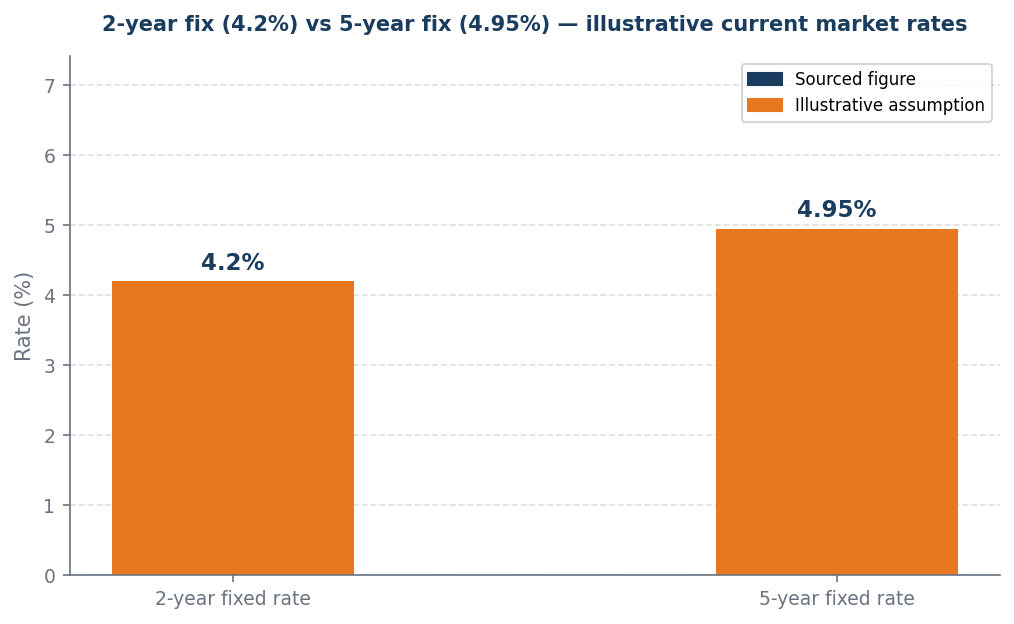

The rate comparison

The rate gap between 2-year and 5-year fixes has narrowed since 2021 — the certainty premium on the 5-year is historically low.

The 0.75 percentage point rate gap between the 4.2% 2-year fixed rate and the 4.95% 5-year fixed rate indicates a significant cost saving that outweighs the certainty premium associated with locking in a longer-term rate. Choosing the 2-year fix allows for a lower initial payment, which can be reinvested or used to offset potential rate increases at the next refixing event, making the financial impact more favorable. The material savings from the lower rate justify the risk of having to refix twice, as the potential for lower rates in the future could further enhance overall savings. Therefore, the 2-year fix is the optimal choice for maximizing financial efficiency in this scenario.

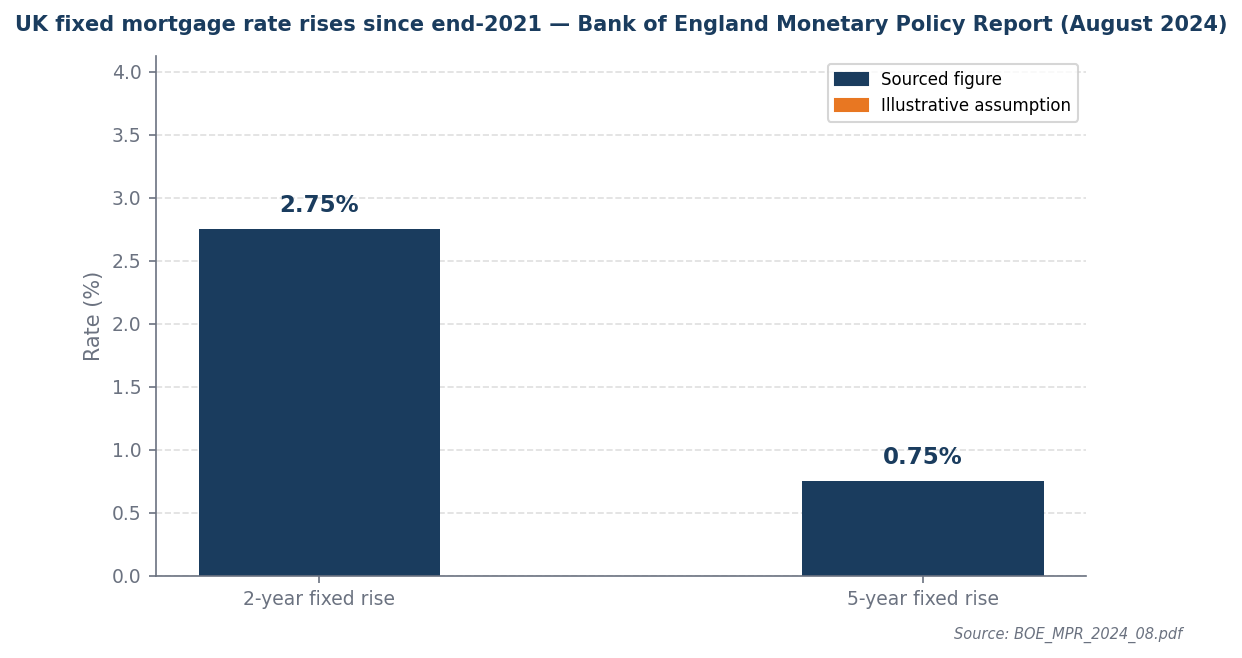

The rate backdrop

2-year fixed rates rose 2.75pp since 2021 versus only 0.75pp for 5-year fixes — the short end absorbed most of the shock.

Bank of England data indicates a significant divergence in fixed-rate mortgage trends since 2021, with 2-year fixed rates increasing by 2.75 percentage points compared to a mere 0.75 percentage point rise in 5-year fixed rates. This 0.75 percentage point gap highlights the relative cost-effectiveness of opting for a 2-year fixed rate, as the substantial savings realized can outweigh the potential risks associated with two refixing events. Consequently, borrowers may find that the shorter-term commitment of a 2-year fix not only offers immediate financial relief but also positions them advantageously in a fluctuating interest rate environment.

Worked example

Assumptions (illustrative): £200,000 mortgage · 4.2% 2-year fix · 4.95% 5-year fix · 5-year comparison horizon

At these rates, the 2-year fix costs £81/month less than the 5-year fix (£1,074 vs £1,155).

| Year | 2yr fix payment | 5yr fix payment | Cumulative difference |

|---|---|---|---|

| Year 1 | £1,074/month | £1,155/month | 2yr saves £972 over 1yr |

| Year 2 | £1,074/month | £1,155/month | 2yr saves £1,944 over 2yr |

| Year 3 | £1,074/month | £1,155/month | 2yr saves £2,916 over 3yr |

| Year 4 | £1,074/month | £1,155/month | 2yr saves £3,888 over 4yr |

| Year 5 | £1,074/month | £1,155/month | 2yr saves £4,860 over 5yr |

Over 5 years, the 2-year fix saves £4,860 — but this assumes the rate gap persists and you refix at a similar rate.

If you need to exit the 5-year fix early, the ERC is approximately £4,000 (2.0% of balance). Factor this into the decision if your situation may change.

When this flips

This flips only when the rate gap between 2-year and 5-year fixes exceeds 0.5pp consistently. Below this threshold, the 5-year certainty premium wins.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Rate gap is large and 2yr is materially cheaper | Take the 2-year fix | £81/month saving compounds over 2 years — the cost case is clear |

| You value certainty above cost | Take the 5-year fix | The premium buys you 5 years without a refix event or rate risk |

| You expect rates to fall further within 2 years | Take the 2-year fix | You capture today's saving and refix at a lower rate in 2 years |

| Uncertain outlook | Take the 2-year fix | The gap is too wide to pay the 5yr premium without a strong certainty reason |

Sources and provenance

- boe_mpr_2026_02.pdf

- OECD_EO_116.pdf

Data as of: 2026-04-08

Find your best mortgage rate — free broker

This article contains affiliate links. We may earn a commission if you click through and take out a product. This does not affect our editorial independence or the analysis presented.