Overpay Mortgage or Invest? What the Numbers Say

Verdict

With a 5.5% mortgage and 8.5% expected return, investing has the edge over the long run.

Confidence: High

Break point: This holds while expected returns stay above 5.5% and horizon is at least 10 years.

The rate decision

Overpaying only loses if after-tax returns clear the mortgage hurdle by enough to justify volatility.

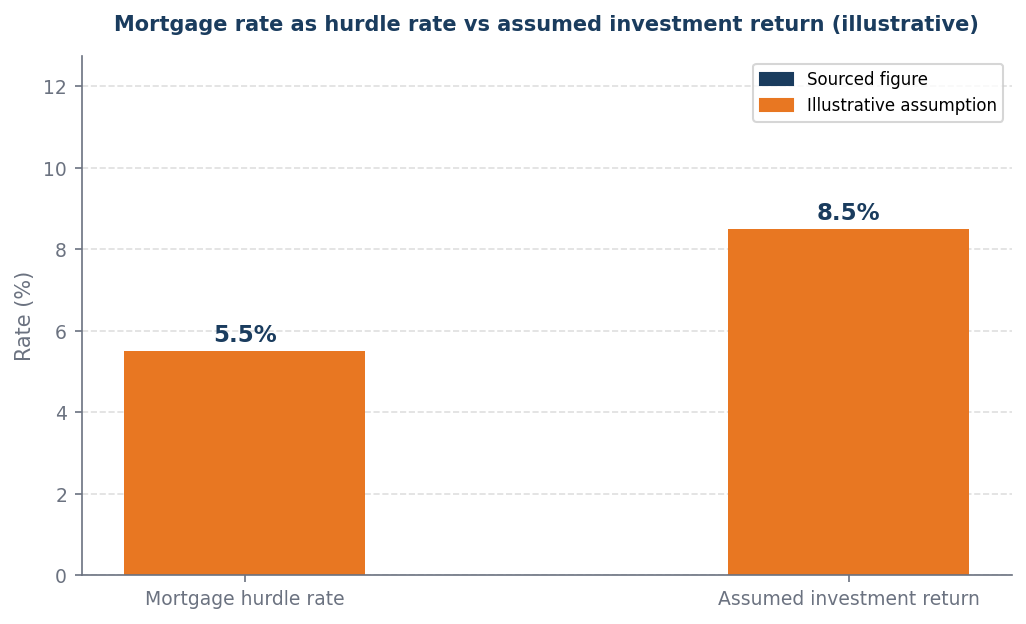

A mortgage rate of 5.5% serves as a hurdle rate, meaning that any investment must yield returns exceeding this rate to be considered advantageous; with an expected return of 8.5%, the investment outpaces the cost of borrowing by a margin of 3.0 percentage points. This gap indicates that funds allocated to investments are likely to generate a higher return than the interest incurred on the mortgage, thereby enhancing overall wealth accumulation. Consequently, leveraging the mortgage to invest is a financially sound strategy, as the returns on investment significantly surpass the cost of financing.

The rate backdrop

Rate rises since 2021 mean the case for overpaying is materially stronger than when mortgage costs were ultra-low.

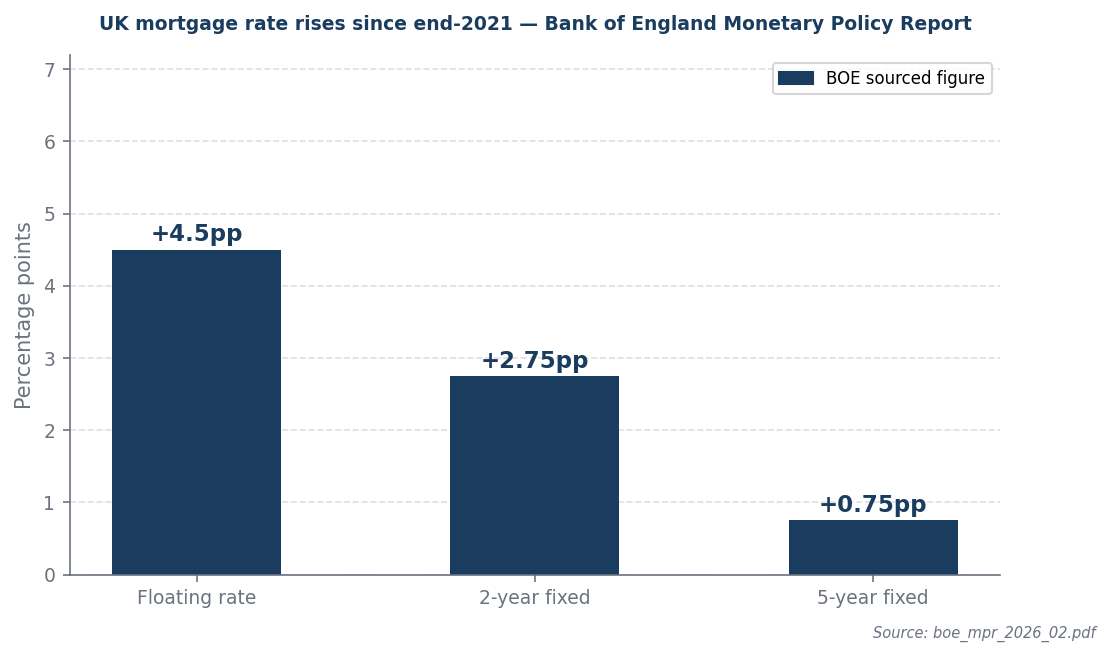

Since 2021, the Bank of England's rate hikes have significantly impacted UK mortgage borrowers, with floating rates increasing by 4.5 percentage points, 2-year fixed rates by 2.75 percentage points, and 5-year fixed rates by 0.75 percentage points, leading to higher borrowing costs. In this context, a mortgage at 5.5% becomes more manageable when juxtaposed with an expected investment return of 8.5%, suggesting that the potential for capital appreciation and income generation from investments outweighs the cost of borrowing. Consequently, this environment favors long-term investment strategies, as the differential between the mortgage rate and expected returns creates a compelling case for leveraging debt to enhance overall portfolio performance.

Worked example

Assumptions (illustrative): £200,000 mortgage · 5.5% rate · £1,000/month spare · 8.5% assumed return

| Year | Overpay saving | Invest profit | Who is ahead |

|---|---|---|---|

| Year 1 | £330 | £479 | Invest profit ahead by £149 |

| Year 2 | £1,320 | £2,060 | Invest profit ahead by £740 |

| Year 3 | £2,970 | £4,843 | Invest profit ahead by £1,873 |

| Year 4 | £5,280 | £8,931 | Invest profit ahead by £3,651 |

| Year 5 | £8,250 | £14,442 | Invest profit ahead by £6,192 |

| Year 6 | £11,880 | £21,501 | Invest profit ahead by £9,621 |

| Year 7 | £16,170 | £30,245 | Invest profit ahead by £14,075 |

| Year 8 | £21,120 | £40,821 | Invest profit ahead by £19,701 |

| Year 9 | £26,730 | £53,394 | Invest profit ahead by £26,664 |

| Year 10 | £33,000 | £68,138 | Invest profit ahead by £35,138 |

By year 10, investment profit is ahead by £35,138.

Risk-adjusted verdict: The 3.0pp gap clears the 1.0pp risk margin — investing is the risk-adjusted winner.

Raw numbers show invest ahead — but the risk margin accounts for investment volatility, sequence-of-returns risk, and the guaranteed nature of mortgage interest saved.

When this flips

This flips only when returns must exceed 6.5% (= 5.5% mortgage rate + 1.0pp margin). The minimum horizon constraint is 10 years.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Return materially above mortgage rate | Invest first | A 3pp+ edge over 10 years compounds to a significant wealth gap |

| Rate above expected return | Overpay first | The hurdle is not cleared — overpaying is the stronger move |

| Uncertain income | Preserve liquidity | Neither path works without a 6-month cash buffer in place |

| Mixed case | Invest majority, overpay remainder | Capture long-run compounding while reducing rate exposure |

Sources and provenance

- boe_mpr_2026_02.pdf

- boe_mpc_2026_03.pdf

Data as of: 2026-04-01