Overpay Mortgage or Invest? What the Numbers Say

Verdict

At 5.5%, overpaying your mortgage is the stronger move right now.

Confidence: High

Break point: This holds while your rate stays above the investment return and horizon is under 3 years.

The rate decision

Overpaying only loses if after-tax returns clear the mortgage hurdle by enough to justify volatility.

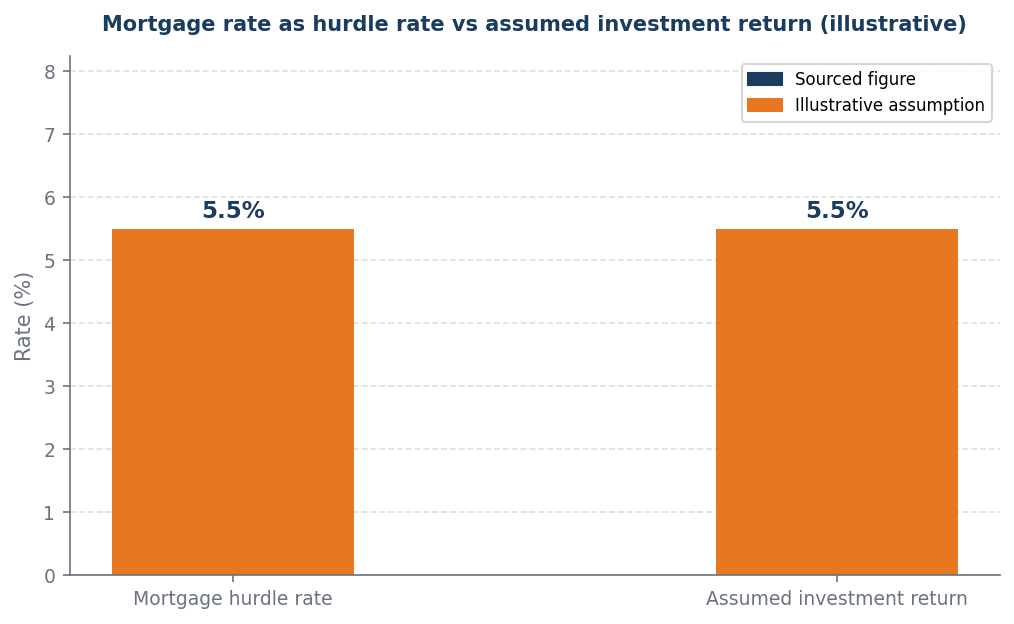

With a mortgage rate of 5.5%, overpaying your mortgage becomes the optimal financial strategy, as this rate serves as a hurdle rate that must be surpassed by any alternative investment returns. Given that the expected investment return is also 5.5%, the gap of 0.0 percentage points indicates that any investment would not yield a superior return compared to the guaranteed savings from reducing your mortgage principal. Therefore, prioritizing mortgage overpayment effectively eliminates interest costs, providing a risk-free return equivalent to the mortgage rate itself. This decisive action enhances your financial position by reducing debt faster and ensuring that your capital is working more efficiently.

The rate backdrop

Rate rises since 2021 mean the case for overpaying is materially stronger than when mortgage costs were ultra-low.

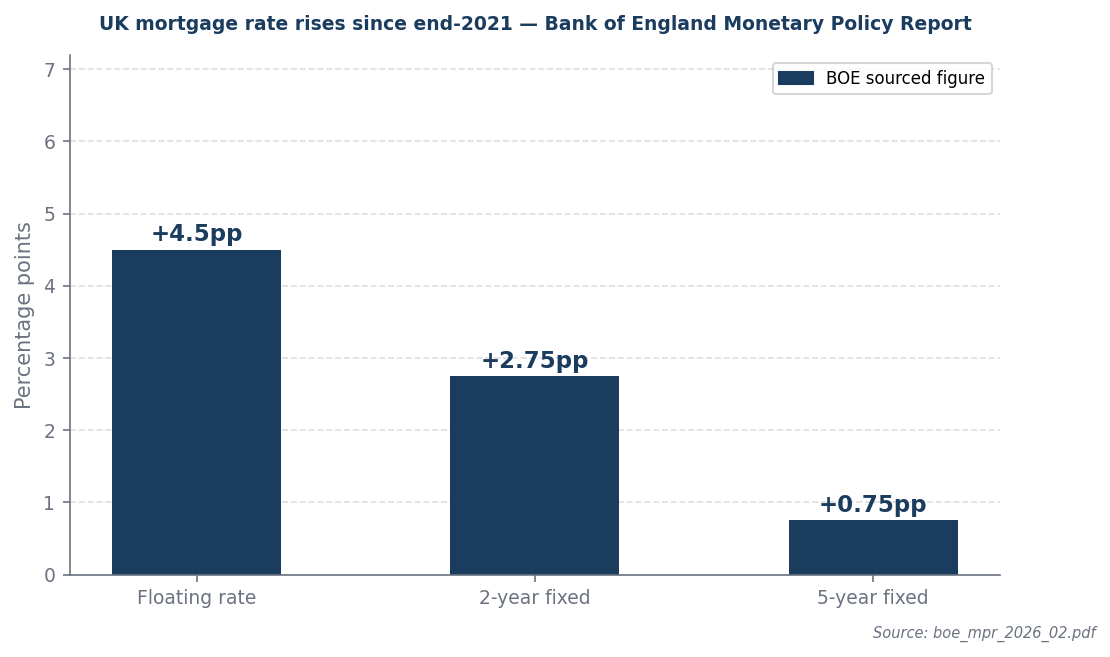

Since 2021, the Bank of England's rate rises have significantly impacted UK mortgage borrowers, with floating rates increasing by 4.5 percentage points, 2-year fixed rates by 2.75 percentage points, and 5-year fixed rates by 0.75 percentage points, leading to higher borrowing costs. In this environment, where the average mortgage rate stands at 5.5%, overpaying your mortgage becomes a financially prudent strategy, as it reduces the principal balance and minimizes interest payments over time, especially given the potential for further rate increases. Additionally, the opportunity cost of holding cash in a low-interest savings account is unfavorable compared to the guaranteed savings from reducing mortgage debt, making overpayment a compelling choice for borrowers seeking to mitigate financial strain.

Worked example

Assumptions (illustrative): £200,000 mortgage · 5.5% rate · £250/month spare · 5.5% assumed return

| Year | Overpay saving | Invest profit | Who is ahead |

|---|---|---|---|

| Year 1 | £82 | £77 | Overpay saving ahead by £5 |

| Year 2 | £330 | £327 | Overpay saving ahead by £3 |

| Year 3 | £742 | £761 | Invest profit ahead by £19 |

By year 3, investment profit is ahead by £19.

Risk-adjusted verdict: The 0.0pp gap does not clear the 2.5pp risk margin — overpaying is the risk-adjusted winner despite invest leading on raw numbers.

Raw numbers show invest ahead — but the risk margin accounts for investment volatility, sequence-of-returns risk, and the guaranteed nature of mortgage interest saved.

When this flips

This flips only when returns must exceed 8.0% (= 5.5% mortgage rate + 2.5pp margin). The minimum horizon constraint is set at 3 years.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Rate above expected return | Overpay first | Certainty of saving outweighs uncertain investment gains at this horizon |

| Low rate with short horizon | Overpay first | 3 years is too short for compounding to overcome volatility |

| Uncertain income | Preserve liquidity | Build 6 months of expenses before committing spare cash either way |

| Mixed case | Overpay first, review in 12 months | Reduce mortgage exposure before taking on investment risk |

Sources and provenance

- boe_mpr_2026_02.pdf

- boe_mpc_2026_03.pdf

Data as of: 2026-04-01