Need flexibility? Why offset beats overpaying every time

Verdict

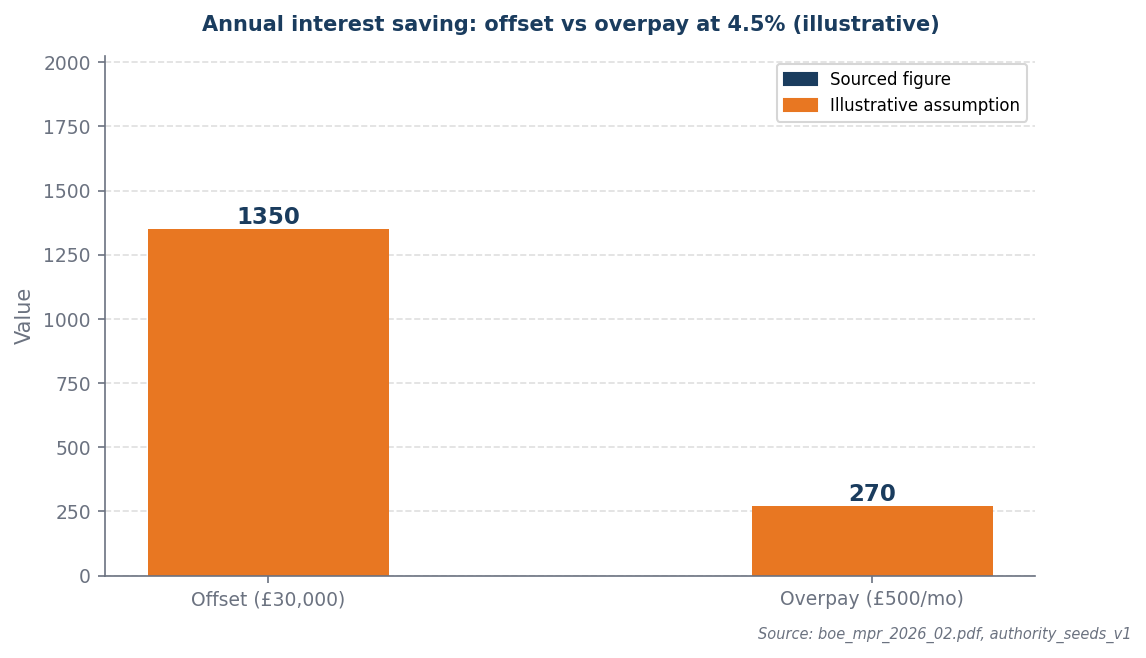

With £30,000 in savings, offset saves £1,350/yr — ahead of monthly overpayments.

Confidence: High

Break point: Offset wins as long as savings balance stays above the overpayment equivalent.

The interest saving

The offset account saves the same interest as overpaying — but keeps your cash accessible, which overpayment does not.

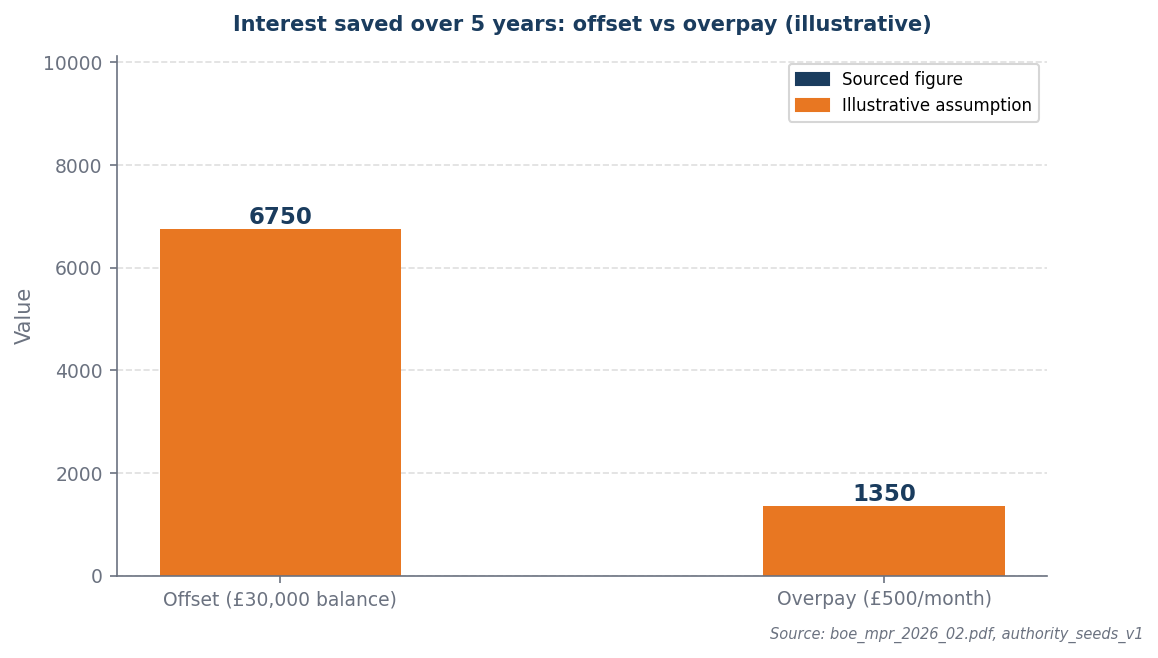

With £30,000 in savings, choosing an offset mortgage saves £1,350 annually compared to making monthly overpayments, both strategies yielding interest savings at 4.5%. The critical factor in this decision is liquidity; if immediate access to funds is paramount for potential emergencies or investment opportunities, the offset option is superior. Conversely, if reducing the mortgage balance is prioritized to minimize long-term interest payments, monthly overpayments may be more advantageous. Ultimately, the choice hinges on whether the flexibility of accessible savings outweighs the benefits of a lower mortgage balance.

The liquidity trade-off

Both strategies save identical interest — the offset keeps cash accessible where overpayment does not.

In a mortgage rate environment of 4.5%, both overpaying and offsetting become attractive strategies primarily due to the focus on liquidity rather than return on investment. With £30,000 in savings, utilizing an offset account can save £1,350 annually in interest payments, which is more advantageous than making monthly overpayments that tie up cash flow and reduce liquidity. This approach allows homeowners to maintain access to their savings while still benefiting from interest savings, making offsetting a more flexible and financially prudent choice in this context. The ability to retain liquidity while minimizing interest costs positions offsetting as the superior strategy in a high-rate mortgage landscape.

Worked example

Assumptions (illustrative): £200,000 mortgage · 4.5% rate · £30,000 offset · £500/month overpayment

| Strategy | Annual saving | 5-year saving | Cash accessible |

|---|---|---|---|

| Offset (£30,000) | £1,350 | £6,750 | Yes — instantly |

| Overpay (£500/month) | £270 | £1,350 | No — locked in |

Over 5 years, offset saves £5,400 more. The offset keeps £30,000 fully accessible.

When this flips

This flips only when the savings balance changes materially or the need for liquidity changes. At 4.5%, both strategies save identical interest — only liquidity need determines the winner.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Liquidity is primary concern | Offset account only | Overpayment locks cash — offset keeps it accessible |

| Expecting large expenditure | Keep savings in offset | Offset allows withdrawal at any time unlike overpayment |

| Variable income | Offset as buffer and saver | Dual purpose: interest saving and emergency fund |

| Rate sensitivity | Offset adapts automatically | Saving scales with rate — no action needed when rates change |

Sources and provenance

- boe_mpr_2026_02.pdf

- authority_seeds_v1

Data as of: 2026-04-01