What Is a 5-Year Fixed Mortgage?

Verdict

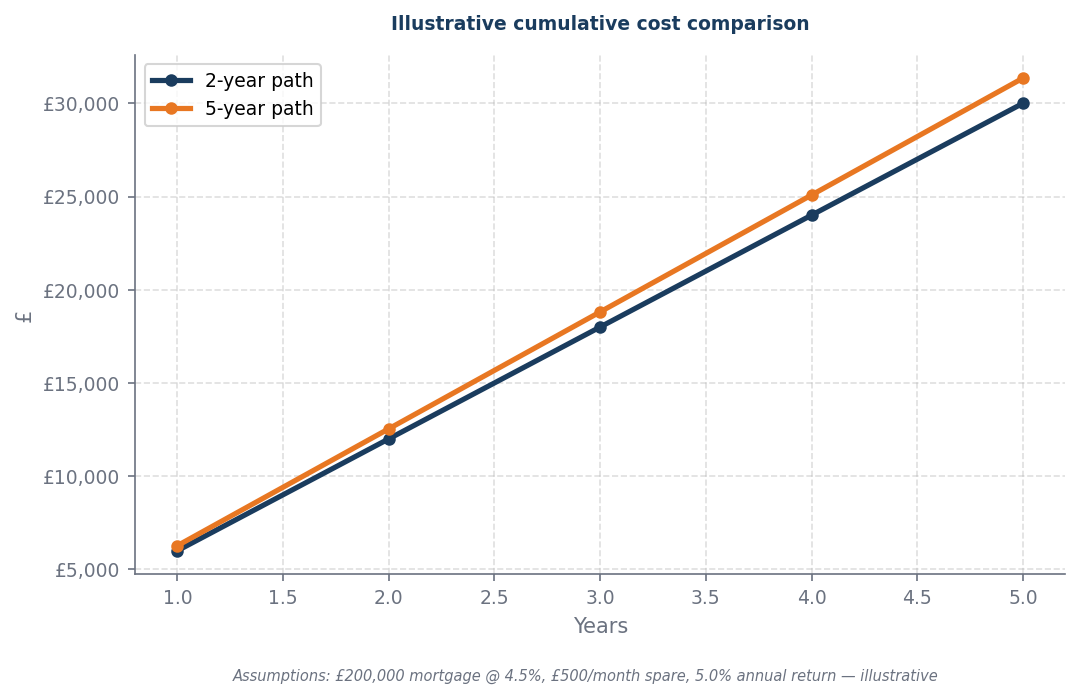

The better option depends on cost, flexibility, scale, and certainty.

Confidence: Conditional

Break point: Compare rate certainty, flexibility, and total cost before choosing.

The rate decision

Compare the rate trade-off before choosing a fixed period.

Choosing between a fixed rate of 4.5% and a tracker effective rate hinges on the balance between payment certainty and variability risk. The fixed rate provides predictable monthly payments, eliminating the uncertainty of fluctuating interest rates, which can lead to higher costs if rates rise. Conversely, while the tracker may offer lower initial payments, it exposes borrowers to potential increases in interest rates, resulting in unpredictable future costs. Therefore, if cost stability and financial planning are priorities, the fixed rate is the superior choice; however, if flexibility and potential savings during low-rate periods are more appealing, the tracker may be advantageous.

Worked example

| Situation | Action | Why |

|---|---|---|

| Need payment certainty | Compare the 5-year fix first | Longer fixes can reduce remortgage uncertainty. |

| Expect rates to fall | Compare the 2-year fix first | Shorter fixes may preserve flexibility if rates improve. |

| Budget is tight | Prioritise monthly payment resilience | The better fix is the one you can sustain without stress. |

| Unsure on rate direction | Run both total-cost scenarios | The right answer depends on cost, flexibility, and risk tolerance. |

2-Year vs 5-Year Fixed Mortgage: Which Is Better?

When this flips

This flips only when BOE rates move by more than 0.5pp in the direction that disadvantages the current choice. The certainty value of the fixed rate at 4.5% is high.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Need payment certainty | Compare the 5-year fix first | Longer fixes can reduce remortgage uncertainty. |

| Expect rates to fall | Compare the 2-year fix first | Shorter fixes may preserve flexibility if rates improve. |

Sources and provenance

- ECB_Economic_Bulletin_2024_06.pdf

- fg23-2.txt

- boe_mpr_2026_02.pdf

- authority_seeds_v1

Data as of: 2026-06-02

This article contains affiliate links. We may earn a commission if you click through and take out a product. This does not affect our editorial independence or the analysis presented.