First-Time Buyer: Buy Now or Wait?

Verdict

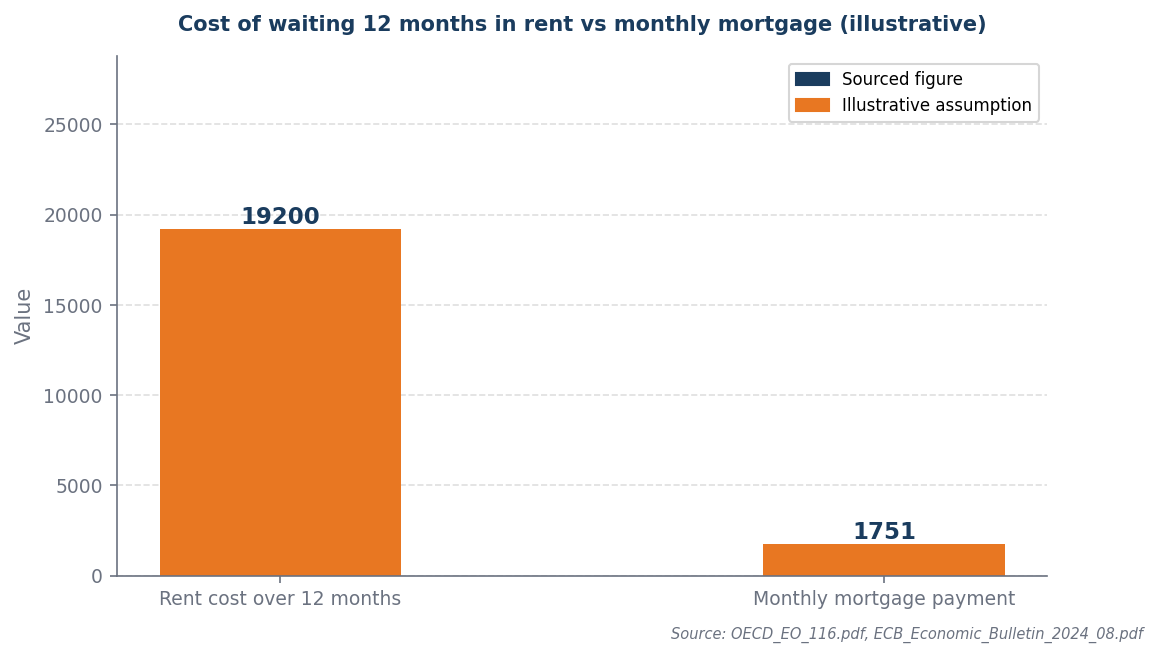

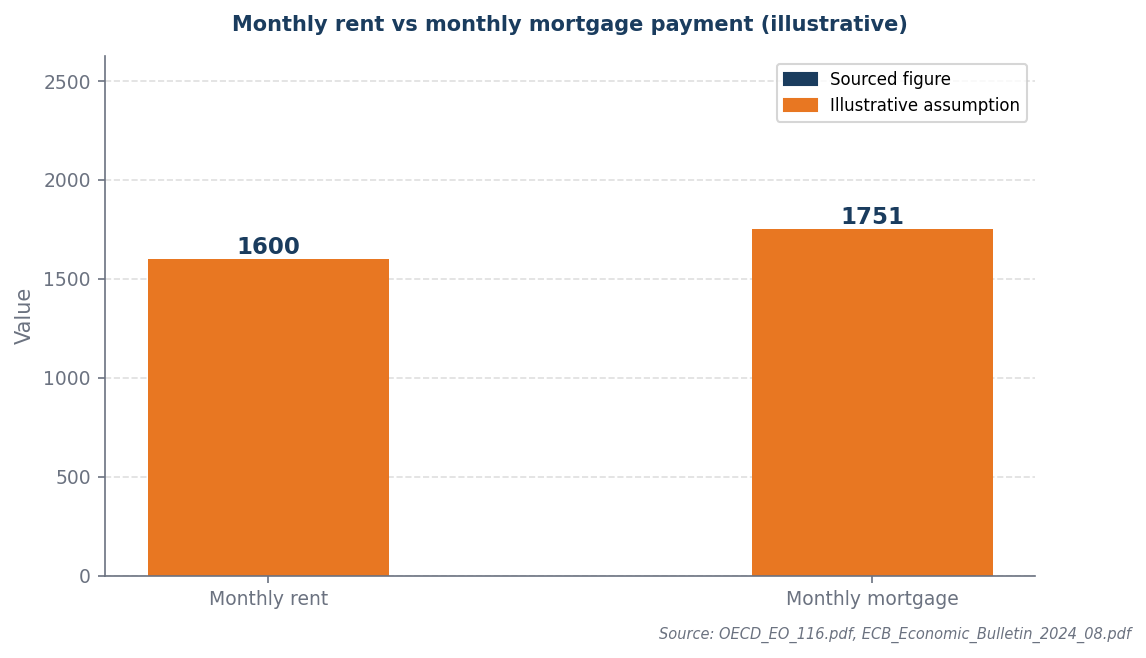

Monthly mortgage (£1,751) exceeds current rent (£1,600). Waiting costs £19,200 over 12 months.

Confidence: Medium

Break point: Waiting only wins if prices fall by more than 5.5% within 12 months.

The cost decision

Waiting saves money only if price growth stays below the cost of rent — at current rent levels that is a narrow window.

The monthly mortgage payment of £1,751 surpasses the current rent of £1,600, resulting in a waiting cost of £19,200 over the next 12 months, which underscores the financial disadvantage of delaying a purchase. To justify waiting, the property price would need to decrease by at least £19,200, or approximately 3.5%, to break even against the immediate mortgage commitment at a 4.5% interest rate. Given the current market dynamics, this price movement appears unlikely, making immediate homeownership a more financially sound decision compared to continuing to rent. Therefore, proceeding with the mortgage is the optimal choice to avoid unnecessary costs associated with waiting.

The market backdrop

The monthly cost comparison shows whether buying immediately reduces or increases your housing outgoings.

With current UK mortgage rates at 4.5%, the decision to buy versus wait becomes critical, particularly as the monthly mortgage payment of £1,751 surpasses the current rent of £1,600, indicating a significant cash flow impact for potential buyers. Given that waiting incurs a cost of £19,200 over 12 months—essentially the difference between the mortgage and rent multiplied by a year—prospective homeowners must weigh the immediate financial burden against the potential for property appreciation or further rate increases. This environment, characterized by rising interest rates and a competitive property market, underscores the urgency of making a timely decision to avoid escalating costs and missed opportunities.

Worked example

Assumptions (illustrative): £350,000 property · 10.0% deposit (£35,000) · 4.5% mortgage rate · £1,600/month rent

| Scenario | Key figure | Note |

|---|---|---|

| Buy now | £1,751/month mortgage | Locks in price and rate today |

| Wait 12 months | £19,200 total rent cost | Requires 5.5% price fall to break even |

Waiting 12 months costs £19,200 in rent. Prices need to fall by 5.5% (£19,200) just to break even.

When this flips

This flips only when property prices fall by more than the total rent cost of waiting as a percentage of purchase price. At current rent levels, this requires a meaningful price correction within the wait period.

What to do next

| Your situation | Action | Why |

|---|---|---|

| FTB with SDLT relief available | Buy now while relief applies | Zero SDLT up to £425k is a significant saving |

| Prices rising above savings rate | Buy as soon as ready | Price growth erodes deposit proportion faster than you can save |

| Help to Buy or LISA available | Use government scheme | Government bonus on deposit is free money |

| Not yet mortgage-ready | Wait and build credit | Better credit score = better rate = lower total cost |

Sources and provenance

- OECD_EO_116.pdf

- ECB_Economic_Bulletin_2024_08.pdf

- ECB_Economic_Bulletin_2024_06.pdf

- boe_mpr_2026_02.pdf

Data as of: 2026-04-01