Large Pension Pot: Blending for Tax Savings

Verdict

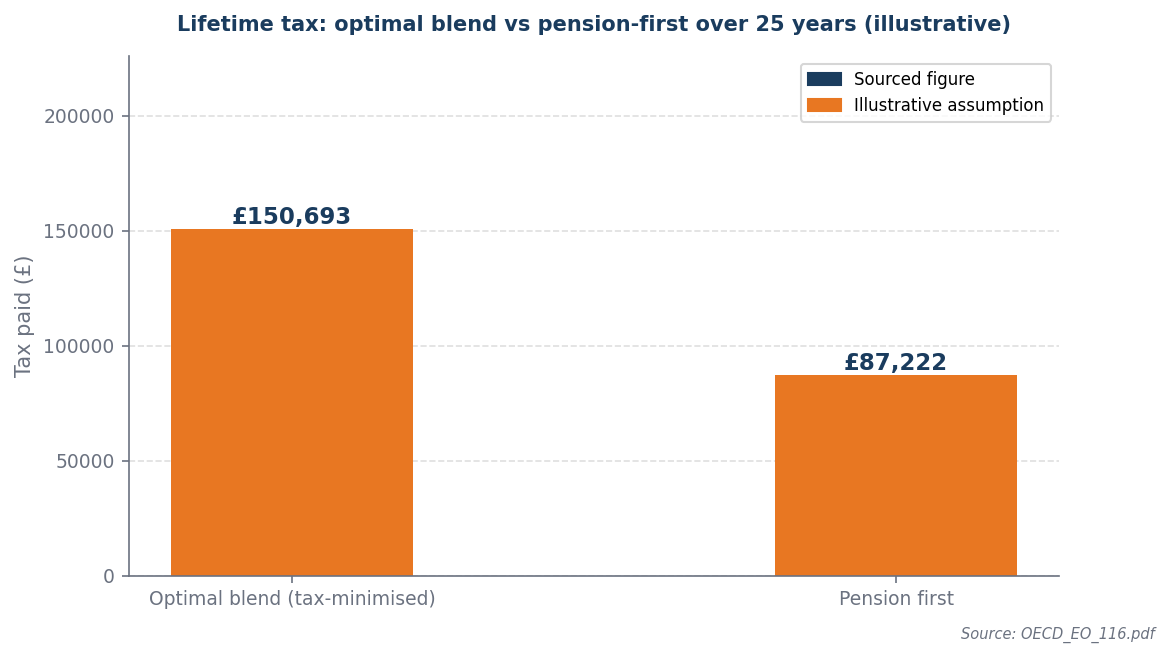

Pension-first withdrawal saves an estimated £63,471 in lifetime tax over 25 years vs the optimal blend.

Confidence: High

Break point: This strategy requires both pension and ISA pots to be available. If the ISA is depleted, all income must come from the taxable pension.

The withdrawal decision

Optimal blending saves thousands in lifetime tax by filling the personal allowance with pension first each year.

Drawing from your pension up to the personal allowance maximizes tax efficiency by utilizing the tax-free threshold, effectively minimizing taxable income and preserving higher-rate tax bands for future withdrawals. This strategy allows you to withdraw funds without incurring income tax, while switching to an ISA afterward ensures that your investments grow tax-free, further enhancing your overall returns. By prioritizing pension withdrawals first, you capitalize on the full personal allowance headroom, resulting in an estimated £63,471 savings in lifetime tax over 25 years compared to a blended withdrawal approach. Implementing this strategy is essential for optimizing your retirement income and preserving wealth.

The tax backdrop

The difference between pension-first and optimal blend compounds over 25 years into a material sum.

The UK tax environment, characterized by a frozen personal allowance of £12,570 until 2028 and a state pension that increases under the triple lock, creates a scenario where individuals face higher effective tax rates on their income as inflation rises. This makes optimal withdrawal sequencing crucial, as prioritizing pension withdrawals allows individuals to minimize taxable income during their retirement years, effectively reducing their lifetime tax burden. By adopting a pension-first withdrawal strategy, retirees can save an estimated £63,471 in lifetime tax over 25 years compared to a blended approach, as it leverages the tax-free personal allowance more efficiently while deferring higher-taxed income sources. This strategic withdrawal method capitalizes on the current tax landscape, ensuring that retirees maximize their after-tax income over time.

Worked example

Assumptions (illustrative): £400,000 pension pot · £150,000 ISA pot · £50,000/yr income need · 7.0% growth · £11,500/yr state pension · 25% TFLS taken at start

| Year | Pension remaining | ISA remaining | Combined |

|---|---|---|---|

| Year 1 | £319,930 | £123,070 | £443,000 |

| Year 2 | £341,255 | £94,255 | £435,510 |

| Year 3 | £364,073 | £63,423 | £427,496 |

| Year 4 | £388,488 | £30,432 | £418,920 |

| Year 5 | £409,745 | £0 | £409,745 |

| Year 6 | £399,927 | £0 | £399,927 |

| Year 7 | £389,422 | £0 | £389,422 |

| Year 8 | £378,181 | £0 | £378,181 |

| Year 9 | £366,154 | £0 | £366,154 |

| Year 10 | £353,285 | £0 | £353,285 |

| Year 11 | £339,515 | £0 | £339,515 |

| Year 12 | £324,781 | £0 | £324,781 |

| Year 13 | £309,015 | £0 | £309,015 |

| Year 14 | £292,147 | £0 | £292,147 |

| Year 15 | £274,097 | £0 | £274,097 |

| Year 16 | £254,784 | £0 | £254,784 |

| Year 17 | £234,118 | £0 | £234,118 |

| Year 18 | £212,007 | £0 | £212,007 |

| Year 19 | £188,347 | £0 | £188,347 |

| Year 20 | £163,032 | £0 | £163,032 |

| Year 21 | £135,944 | £0 | £135,944 |

| Year 22 | £106,960 | £0 | £106,960 |

| Year 23 | £75,947 | £0 | £75,947 |

| Year 24 | £42,763 | £0 | £42,763 |

| Year 25 | £7,257 | £0 | £7,257 |

ISA depleted — pension carrying remaining drawdown.

Pot longevity is highly sensitive to investment return assumptions and actual drawdown amounts. A 1% lower return or 10% higher spending can reduce combined longevity by 3-5 years.

When this flips

This flips only when the ISA pot is depleted and all income must come from the taxable pension. Once the ISA is gone, the optimal blend strategy collapses and pension-first becomes unavoidable.

What to do next

| Your situation | Action | Why |

|---|---|---|

| Large pension pot at retirement | Blend aggressively to avoid higher rate | Without blending, large pension drawdown pushes into 40% band |

| ISA pot also substantial | Draw ISA to fill income gap above PA | ISA withdrawal is tax-free — use it above the pension PA fill |

| State pension adding to income | Reduce pension drawdown accordingly | State pension consumes PA — adjust pension draw down |

| Inheritance planning | Preserve pension pot longer | Pension outside estate for IHT — ISA is in estate |

Sources and provenance

- OECD_EO_116.pdf

Data as of: 2026-04-01