Ditch Your Fixed Rate Mortgage Early? Here's What to Know

Verdict

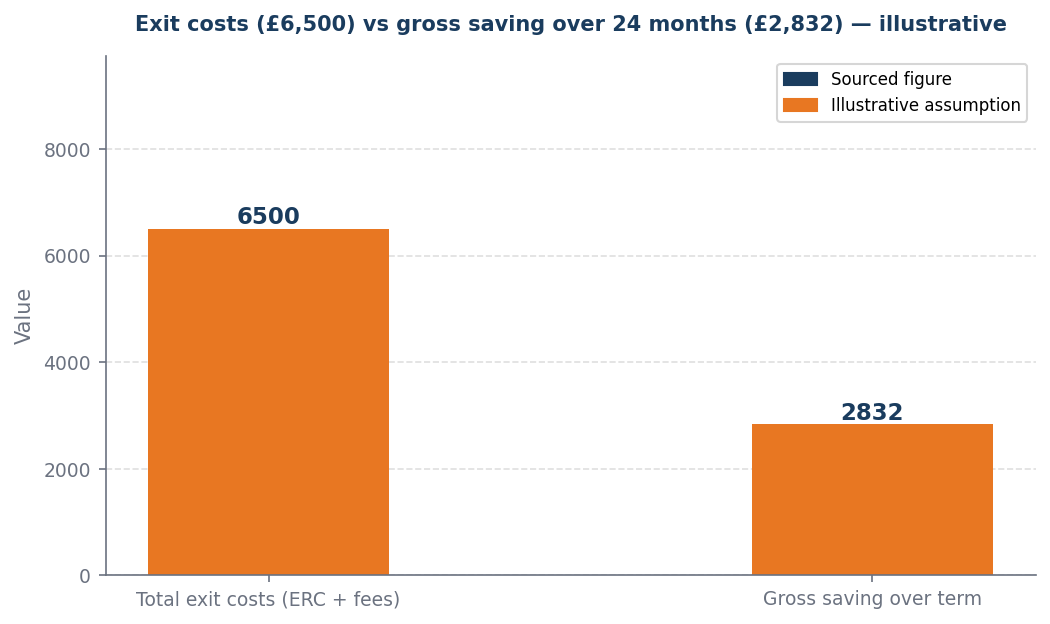

With ERC and switch costs of £6,500 exceeding the £2,832 saving over 24 months, staying in your 5.5% fix is the stronger move.

Confidence: High

Break point: This verdict flips if the rate gap widens materially or ERC drops below 3.0%. The break-even point is 55.1 months of saving — only viable if you have that long remaining.

The exit cost decision

Ditching only makes sense when the gross saving over the remaining term exceeds the ERC and switch costs.

The £6,500 early repayment charge (ERC) is a one-time cost that significantly outweighs the £2,832 savings from switching to a 4.5% rate over 24 months, making it financially imprudent to switch. The 1.0 percentage point gap between your current 5.5% fixed rate and the available 4.5% rate means that while the monthly savings may seem attractive, they do not compensate for the substantial upfront cost of the ERC. Therefore, remaining in your current 5.5% fixed rate is the stronger financial decision, as it avoids the immediate financial burden of the ERC while providing stability in your mortgage payments.

The rate backdrop

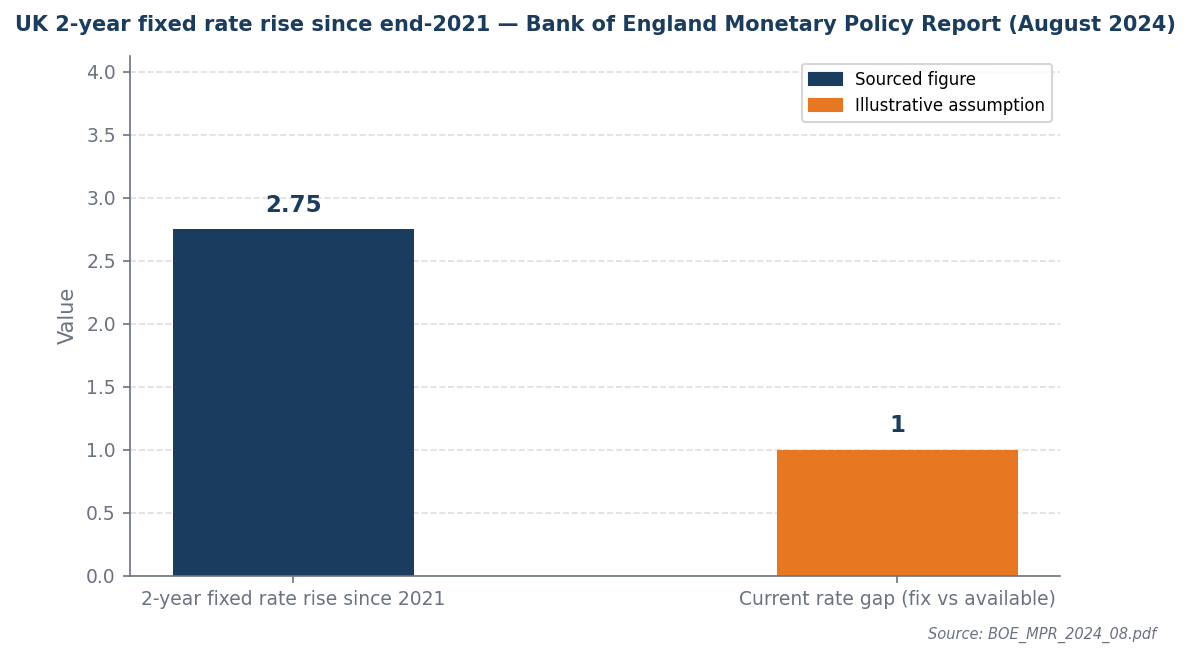

Borrowers who fixed at the 2022-23 peak are paying well above current market rates, so the case for exiting has strengthened.

Since 2021, the Bank of England's rate rises have significantly impacted the borrowing landscape, with 2-year fixed rates increasing by 2.75 percentage points from historic lows, making refinancing less attractive for those still on high fixed rates. For borrowers facing early repayment charges (ERC) and switching costs averaging £6,500, the potential savings of £2,832 over 24 months from moving to a lower rate are insufficient to justify the immediate financial burden of switching. Consequently, remaining in a 5.5% fixed rate is the more prudent choice, as it avoids the substantial upfront costs associated with refinancing while providing stability in an uncertain interest rate environment.

Worked example

Assumptions (illustrative): £200,000 mortgage · 5.5% current fix · 4.5% available rate · 24 months remaining · 3.0% ERC

| Item | Amount |

|---|---|

| Monthly saving | £118/month |

| Gross saving over 24 months | £2,832 |

| Early repayment charge (3.0%) | −£6,000 |

| Switch costs | −£500 |

| Net saving | −£3,668 |

Staying in the fix saves £3,668 compared to ditching — the exit costs of £6,500 are not recovered within the 24-month remaining term.

This flips if ERC drops below 1.17% or if the monthly saving increases above £271/month.

When this flips

This flips only when the net saving after ERC and switch costs exceeds the break-even threshold. Below this threshold, the certainty of staying in the fix wins.

What to do next

| Your situation | Action | Why |

|---|---|---|

| ERC is 3% or above | Stay in the fix | A £6,000 exit penalty needs an exceptional rate gap to break even |

| Rate gap is large and remaining term is long | Calculate the break-even carefully | A 2pp+ gap over 36+ months can overcome even a large ERC — check the numbers |

| You plan to move within the fix period | Check mortgage portability terms | A portable mortgage avoids the ERC entirely — verify before assuming you must pay it |

| Uncertain | Stay in the fix and review in 6 months | Unless rates fall significantly further, the ERC makes ditching hard to justify |

Sources and provenance

- boe_mpr_2026_02.pdf

- boe_mpc_2026_03.pdf

Data as of: 2026-04-01